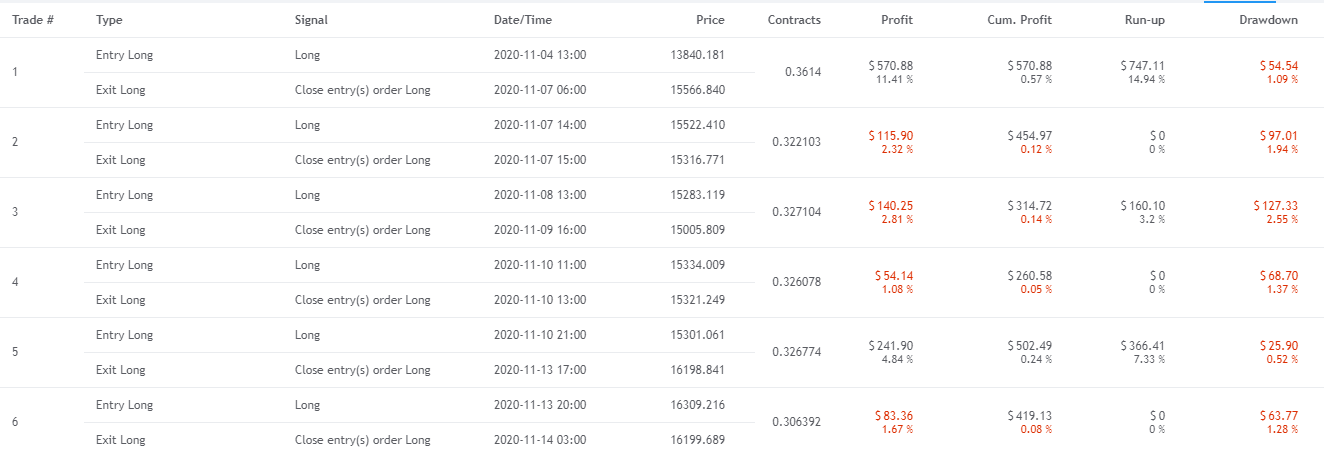

I tried to backtest a simple strategy on TradingView, it made 6 trades with these results:

Now I want to calculate Sharpe ratio using definition provided by TradingView.

So, my daily returns(

Now I want to calculate Sharpe ratio using definition provided by TradingView.

So, my daily returns(profit_by_days) equals:

2020-11-07 0.45

2020-11-08 0.00

2020-11-09 -0.14

2020-11-10 -0.05

2020-11-11 0.00

2020-11-12 0.00

2020-11-13 0.24

2020-11-14 -0.08

Using this Pandas code:

sharpe = (profit_by_days.mean() - (2/365))/profit_by_days.std(ddof=0)

I get 0.257 Sharpe ratio, while TradingView shows 0.205.

Why did I get a different result?

(absolute_profit_of_trade * 100) / capital. What do you mean byamdandbp? $\endgroup$