I'm having a problem getting options data with IB's API. The data seems not to be correct. In my code I'm getting some 0DTE call options for the Mini SP500 March Futures contract and printing their bid, ask and delta. For this I'm using the ib_sync which simplifies development greatly. This is the code:

from datetime import datetime

from ib_insync import *

import pandas as pd

import math

from datetime import datetime, time

def week_of_month(dt):

""" Returns the week of the month for the specified date.

"""

first_day = dt.replace(day=1)

dom = dt.day

adjusted_dom = dom + first_day.weekday()

return int(math.ceil(adjusted_dom/7.0))

def get_trading_class(dt: datetime):

week = week_of_month(dt)

day = dt.weekday()

res = 'E' + str(week)

if day == 4:

return 'EW' + str(week)

else:

return 'E' + str(week) + chr(60+day)

ib = IB().connect('winhost', 7496, clientId=123, timeout=15)

es = Future('ES', '202303', 'CME')

print(ib.qualifyContracts(es))

ib.reqMarketDataType(1)

[ticker] = ib.reqTickers(es)

# spx current price

spxValue = ticker.marketPrice()

print('es futue value: ', spxValue)

chains = ib.reqSecDefOptParams(es.symbol, 'CME', es.secType, es.conId)

# chainsDf = util.df(chains)

# print(chainsDf.to_string(max_colwidth=10))

# chainsDf = chainsDf[(chains.exchange == 'SMART') & (chains.tradingClass == 'SPXW')]

print('week of the month:', week_of_month(datetime.now()))

trading_cls = get_trading_class(datetime.now())

print('trading class:', trading_cls)

chain = next(c for c in chains if c.tradingClass == trading_cls and c.exchange == 'CME')

expiration = chain.expirations[0]

print('expiration:',expiration)

call_strikes = [strike for strike in chain.strikes

if strike % 5 == 0

and spxValue - 10 < strike < spxValue + 30]

put_strikes = [strike for strike in chain.strikes

if strike % 5 == 0

and spxValue - 30 < strike < spxValue]

rights = ['P', 'C']

contracts = [Option('SPX', expiration, strike, 'C', 'SMART', tradingClass='SPXW') for strike in call_strikes]

contracts = ib.qualifyContracts(*contracts)

tickers = ib.reqTickers(*contracts)

for ticker in tickers:

print('call strike', ticker.contract.strike, 'bid:', ticker.bid, 'ask:', ticker.ask, 'delta:', ticker.lastGreeks.delta)

ib.disconnect()

And this is the output:

[Future(conId=495512572, symbol='ES', lastTradeDateOrContractMonth='20230317', multiplier='50', exchange='CME', currency='USD', localSymbol='ESH3', tradingClass='ES')]

es futue value: 4061.75

week of the month: 3

trading class: EW3

expiration: 20230217

call strike 4055.0 bid: 10.1 ask: 10.3 delta: 0.472330335007325

call strike 4060.0 bid: 7.9 ask: 8.1 delta: 0.3769870767527141

call strike 4065.0 bid: 6.1 ask: 6.3 delta: 0.29022751622672416

call strike 4070.0 bid: 4.6 ask: 4.8 delta: 0.212861073049887

call strike 4075.0 bid: 3.4 ask: 3.6 delta: 0.1491749774504159

call strike 4080.0 bid: 2.55 ask: 2.6 delta: 0.09797399088652259

call strike 4085.0 bid: 1.85 ask: 1.95 delta: 0.06485900831271653

call strike 4090.0 bid: 1.35 ask: 1.4 delta: 0.04255032736417017

I've double checked the price of the contract, and it's correct: 4061.75.

Now, looking at the TWS at the time I make this request, the bid asks and deltas of the options are incorrect. Look at the attached image.

I think I'm getting delayed data, because if the price of the futures contract is 4061.75, the first ITM call option with a delta over 50 should be the 4060, but in my output, the delta for that option is 0.37. Not even the 4055 call is ITM.

So my question is. How is it possible that I'm seeing real time data on the TWS but I'm getting delayed data through the API? Am I missing a Real Time data subscription for the API? In that case, which one?

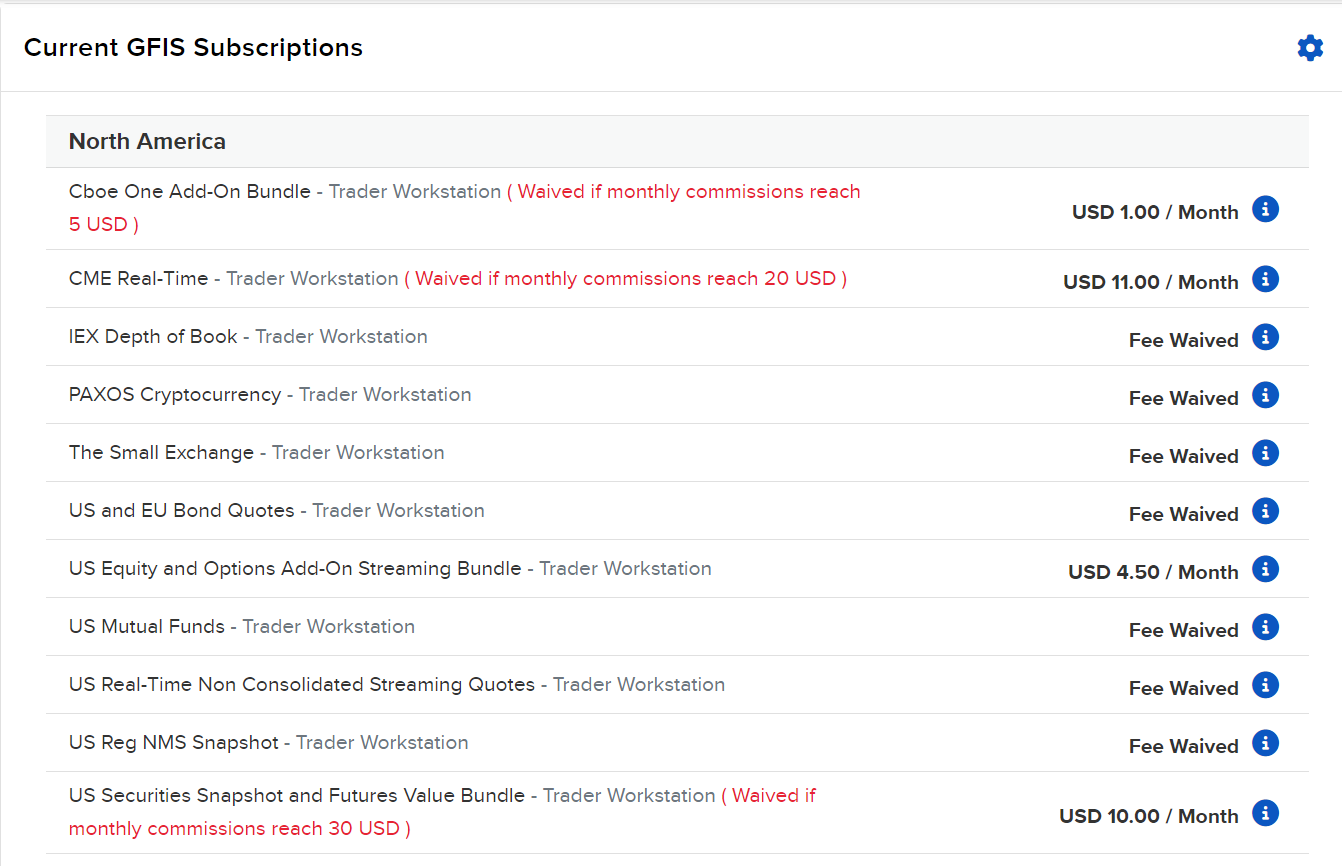

These are my Market Data Subscriptions:

Thanks

ib_insync: groups.io/g/insync $\endgroup$