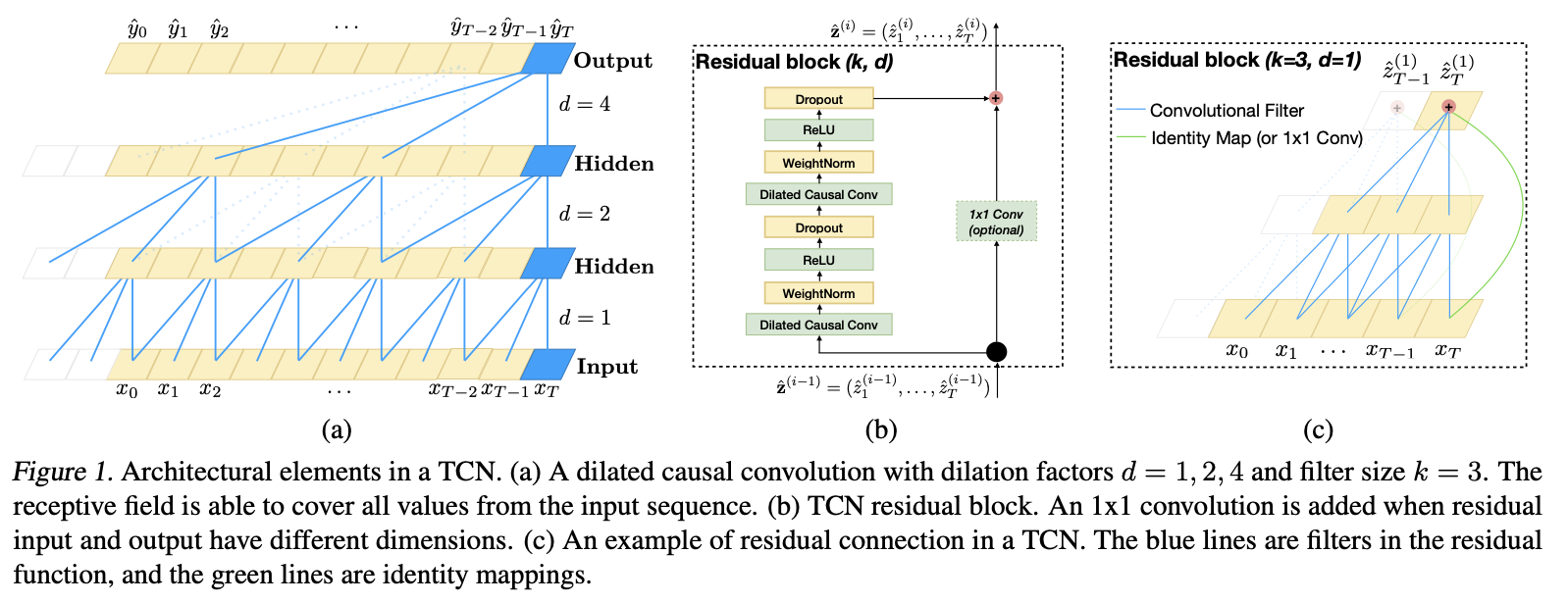

I'm trying to predict the one-day ahead movement of the S&P 500 with Temporal Convolutional Networks 1 to capture some "memory".

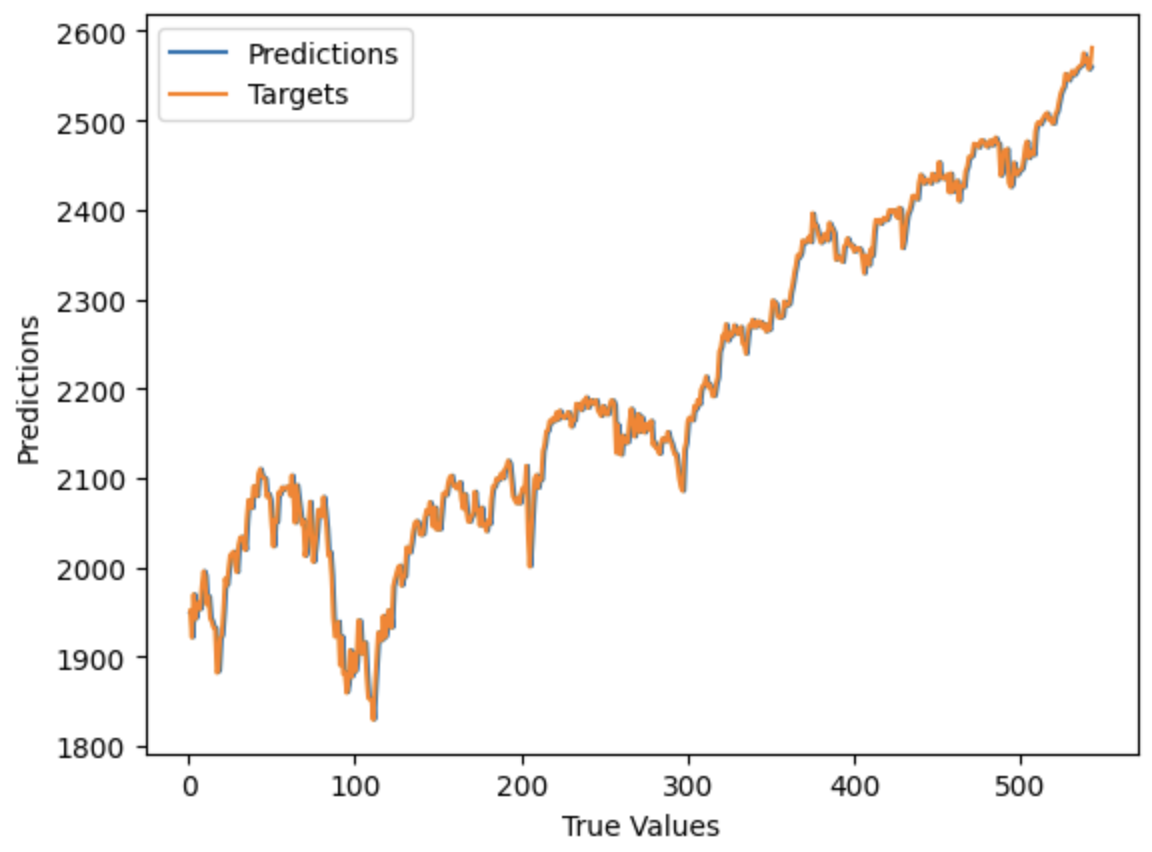

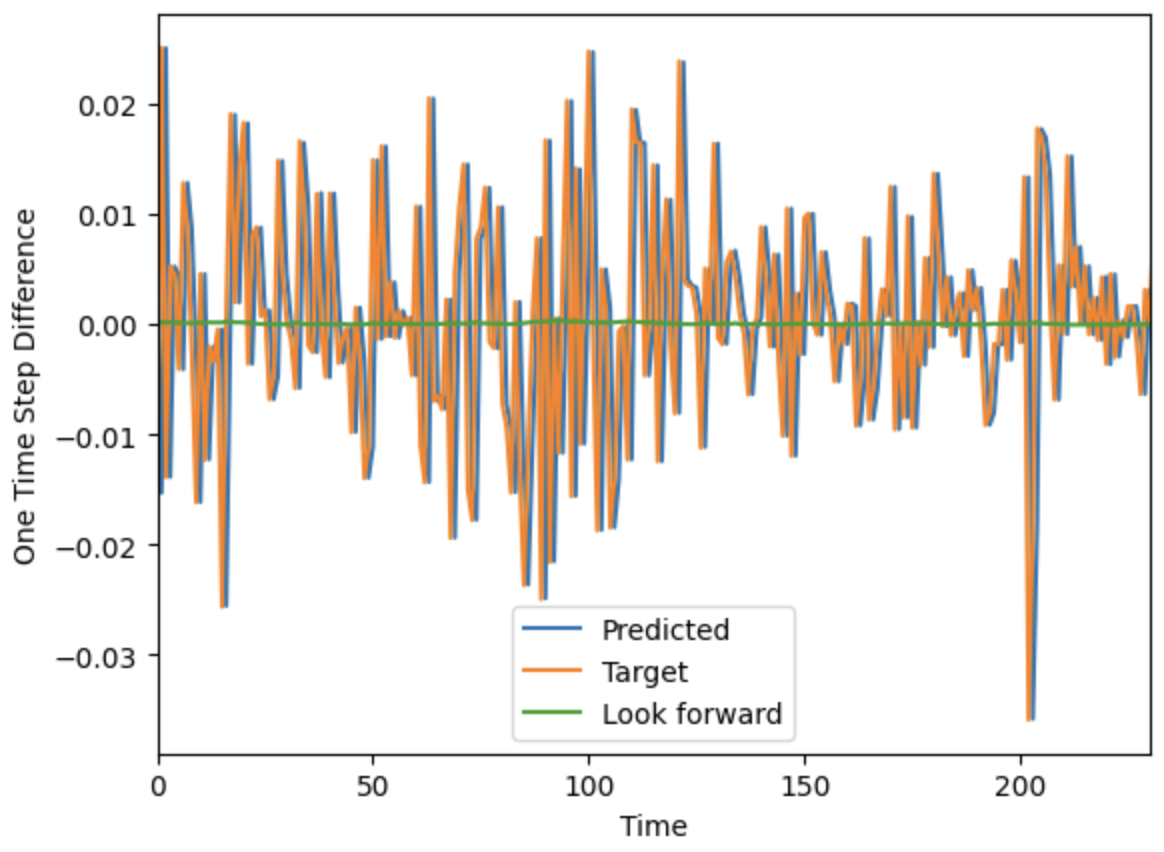

I use daily close data with the loss function $\mathrm{MSE}(f(x_0, \ldots, x_T), y_T)$ where $f(x_0, \ldots, x_T) = \hat y_T := x_{T+1}$ is the output of the neural network. I've tried countless of hyperparameters with this very rudimentary model. But almost all models that do converge close enough converge to the naive estimation of the future closing price by the last known price. I've tried adding more features like VIX and interest rates to no avail.

Otherwise I'm employing early stopping, drop out for regularization, weight normalization for normalization etc and have tried long (almost a year) and short (week) input sequences.

I realize that this is a very rudimentary model and I did not expect anything ground breaking. I want to understand why things behave like they do.

Question:

- Why is it that this network, with the bare minimum of information, convergs to the naive estimation of the last known price?

- How can one make small alterations, perhaps to the loss function or somthing else so it doesn't get "stuck" converging to the naive estimator?