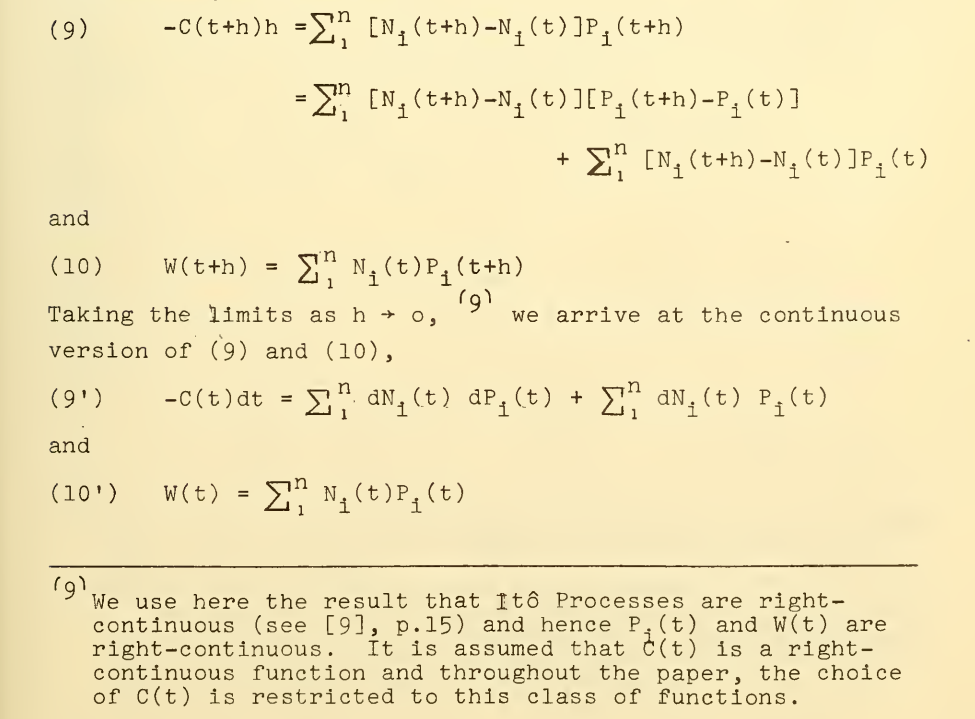

Having to use a typewriter in 1970 Merton tried to find a notation that is as intuitive as possible at the risk of looking unrigorous at first glance. Since the advent of LaTeX it is easy to transcribe his formulas using Riemann-Stieltjes notation as follows (for simplicity I omit the subscripts $i$ in $N$ and $P$

and I won't take the sum over $i\,$):

In the limit, the LHS of Merton's equation (9) can be transcribed in integral form as

$$\tag{a}

-\int_0^t C(s)\,ds\,.

$$

The second line in Merton's equation (9) is the discrete (and differential) analogue of

$$\tag{b}

\lim_{m\to\infty\atop\|\Pi_m|\|\to 0}\sum_{j=1}^{m-1} \big[N(t^m_{j+1})-N(t^m_j)\big]\big[P(t^m_{j+1})-P(t^m_j)\big]

$$

where $0=t^m_1<t^m_2\dots<t^m_m=t$ and $\|\Pi_m\|:=\max\limits_{j=1,\dots,m-1}|t^m_{j+1}-t^m_j|\,.$ Today we call (b)

the quadratic covariation of $N$ and $P$ (see [1]) and denote it by $\langle N,P\rangle_t\,.$ A still popular notation (esp. among physicists) for the

differential $d\langle N,P\rangle_t$ of (b) is $dN\,dP\,.$

The third line of (9) becomes

$$\tag{c}

\lim_{m\to\infty\atop\|\Pi_m|\|\to 0}\sum_{j=1}^{m-1} \big[N(t^m_{j+1})-N(t^m_j)\big]P(t^m_j)

$$

which is the Ito integral $\int_0^t P(s)\,dN(s)\,.$

The first line in Merton's equation (9) is

$$\tag{d}

\lim_{m\to\infty\atop\|\Pi_m|\|\to 0}\sum_{j=1}^{m-1} \big[N(t^m_{j+1})-N(t^m_j)\big]P(t^m_{\color{red}{j+1}})\,.

$$

With a bit of manipulation we can rewrite this as

\begin{align}

&2\lim_{m\to\infty\atop\|\Pi_m|\|\to 0}\sum_{j=1}^{m-1} \big[N(t^m_{j+1})-N(t^m_j)\big]

\frac{P(t^m_{j+1})+P(t^m_j)}{2}\\

&~~-\lim_{m\to\infty\atop\|\Pi_m|\|\to 0}\sum_{j=1}^{m-1} \big[N(t^m_{j+1})-N(t^m_j)\big]

P(t^m_j)\tag{e}

\end{align}

which we recognize as

$$\tag{f}

2\int_0^t P(s)\color{red}{\circ}\,dN(s)-\int_0^t P(s)\,dN(s)

$$

where the first one is a Stratonovich integral and the second again the Ito Integral.

Merton's chain of equations (9) can now be written as

\begin{align}\tag{g}

-\int_0^t C(s)\,ds&=2\int_0^tP(s)\circ dN(s)-\int_0^tP(s)\,dN(s)\\

&=\langle N,P\rangle_t+\int_0^t P(s)\,dN(s)\,.

\end{align}

Corrolary. Merton has (just in a few lines and using a 1970's typewriter) proven the equation

$$\tag{h}

\int_0^t N(s)\circ dP(s)=\int_0^t N(s)\, dP(s)+\frac{1}{2}\langle N,P\rangle_t\,.

$$

(cf. Wikipedia).

I think he should have received the Nobel prize even if he had done nothing else than that.

The treatise of Merton is worth reading because his explanations of what is going on economically in these equations is marvellous.

[1] S. Shreve, Stochastic Calculus for Finance.