I struggle to understand why my market rates does not match my bootstrap model. So I wonder why the spread is that high between market & model.

maturity | market | model

1W | 0.050640 | 0.050626

2W | 0.050670 | 0.050631

3W | 0.050720 | 0.050655

1M | 0.051021 | 0.050916

2M | 0.051391 | 0.051178

3M | 0.051745 | 0.051415

4M | 0.051940 | 0.051493

5M | 0.051980 | 0.051424

6M | 0.051820 | 0.051149

7M | 0.051584 | 0.050821

8M | 0.051310 | 0.050454

9M | 0.050924 | 0.049979

10M | 0.050604 | 0.049582

11M | 0.050121 | 0.049026

12M | 0.049550 | 0.048386

18M | 0.045585 | 0.044806

2Y | 0.042631 | 0.041774

3Y | 0.038952 | 0.038230

4Y | 0.036976 | 0.036321

5Y | 0.035919 | 0.035297

6Y | 0.035350 | 0.034745

7Y | 0.034998 | 0.034403

8Y | 0.034808 | 0.034219

9Y | 0.034738 | 0.034151

10Y | 0.034712 | 0.034125

12Y | 0.034801 | 0.034210

15Y | 0.034923 | 0.034327

20Y | 0.034662 | 0.034075

25Y | 0.033750 | 0.033193

30Y | 0.032826 | 0.032298

40Y | 0.030835 | 0.030369

50Y | 0.028960 | 0.028548

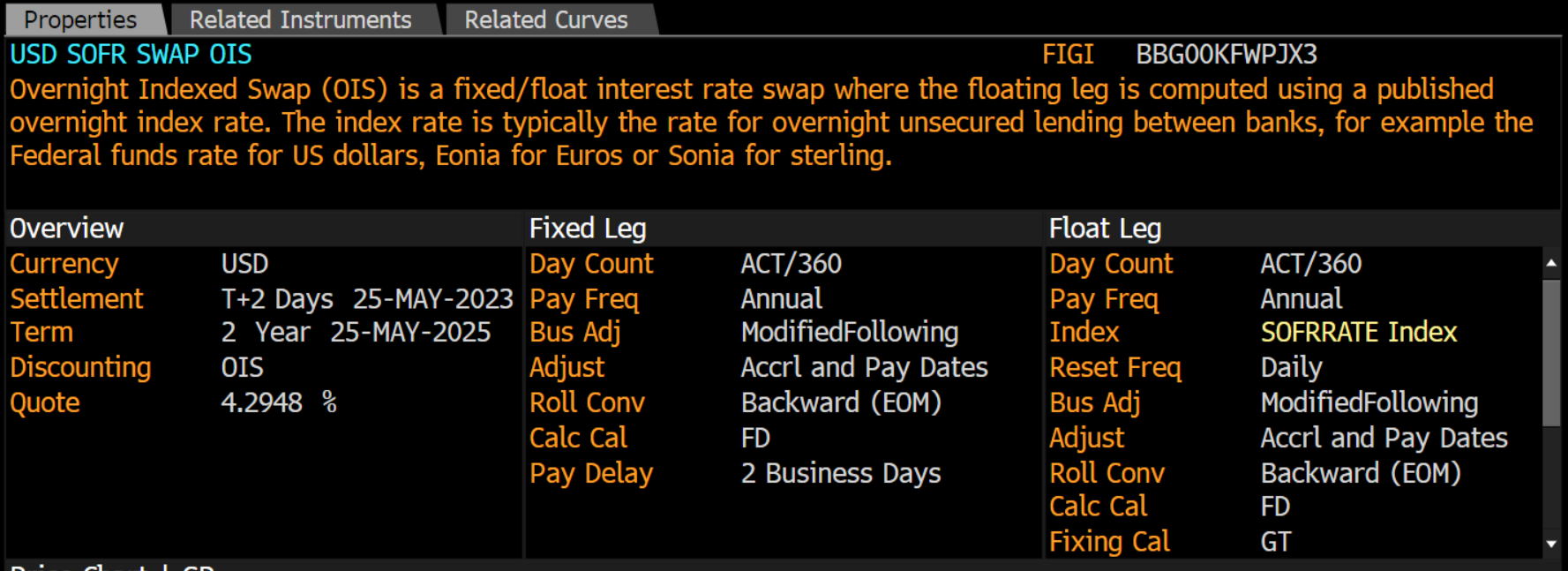

My curve only contain swaps.

Fixed leg :

- Discounting OIS

- Settlement T+2 Days

- Term 2 Week

- Day Count ACT/360

- Pay Freq Annual

- Bus Adj ModifiedFollowing

- Adjust Accrl and Pay Dates

- Roll Conv Backward (EOM)

- Calc Cal FD

- Pay Delay 2 Business Days

Float Leg

- Day Count ACT/360

- Pay Freq Annual

- Index SOFRRATE Index

- Reset Freq Daily

- Bus Adj ModifiedFollowing

self.swaps = {Period("1W"): 0.05064, Period("2W"): 0.05067, Period("3W"): 0.05072, Period("1M"): 0.051021000000000004, Period("2M"): 0.051391, Period("3M"): 0.051745, Period("4M"): 0.05194, Period("5M"): 0.051980000000000005, Period("6M"): 0.051820000000000005, Period("7M"): 0.051584000000000005, Period("8M"): 0.05131, Period("9M"): 0.050924, Period("10M"): 0.050603999999999996, Period("11M"): 0.050121, Period("12M"): 0.049550000000000004, Period("18M"): 0.04558500000000001, Period("2Y"): 0.042630999999999995, Period("3Y"): 0.038952, Period("4Y"): 0.036976, Period("5Y"): 0.035919, Period("6Y"): 0.03535, Period("7Y"): 0.034998, Period("8Y"): 0.034808, Period("9Y"):

0.034738000000000005, Period("10Y"): 0.034712, Period("12Y"): 0.034801, Period("15Y"): 0.034923, Period("20Y"): 0.034662, Period("25Y"): 0.03375, Period("30Y"): 0.032826, Period("40Y"): 0.030834999999999998, Period("50Y"): 0.02896}

Below is how I use OISRateHelper

rate_helpers = []

for tenor, rate in self.swaps.items():

helper = ql.OISRateHelper(2, tenor, ql.QuoteHandle(ql.SimpleQuote(rate)), self.swap_underlying)

rate_helpers.append(helper)

And below is how I compare new rates to given rates :

self.curve = ql.PiecewiseSplineCubicDiscount(calculation_date, rate_helpers, self.swap_day_count_conv)

yts = ql.YieldTermStructureHandle(self.curve)

# Link index to discount curve

index = index.clone(yts)

# Create engine with yield term structure

engine = ql.DiscountingSwapEngine(yts)

# Check the swaps reprice

print("maturity | market | model")

for tenor, rate in self.swaps.items():

swap = ql.MakeVanillaSwap(tenor,

index, 0.01,

ql.Period('0D'),

fixedLegTenor=ql.Period('2D'),

fixedLegDayCount=self.swap_day_count_conv,

fixedLegCalendar=ql.UnitedStates(ql.UnitedStates.GovernmentBond),

floatingLegCalendar=ql.UnitedStates(ql.UnitedStates.GovernmentBond),

pricingEngine=engine)

print(f" {tenor} | {rate:.6f} | {swap.fairRate():.6f}")

Also note that :

self.swap_underlying = ql.OvernightIndex("USD Overnight Index", 2, ql.USDCurrency(), ql.UnitedStates(ql.UnitedStates.Settlement), ql.Actual360())

self.swap_day_count_conv = ql.Actual360()

Did I miss something? Is the implementation I made correct? Are there any discrepancies in the parameters?

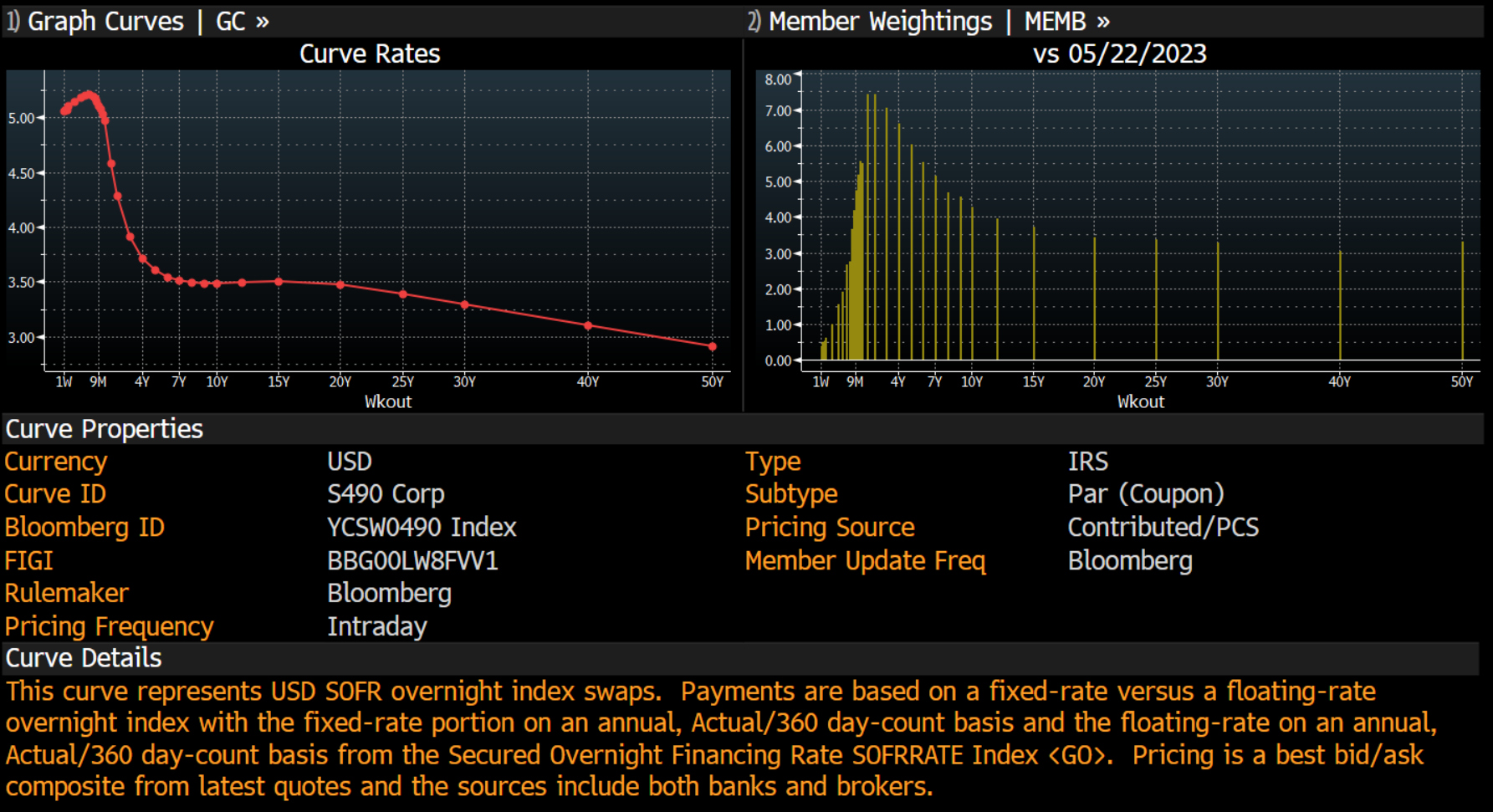

Note Curve description :

Swap description :