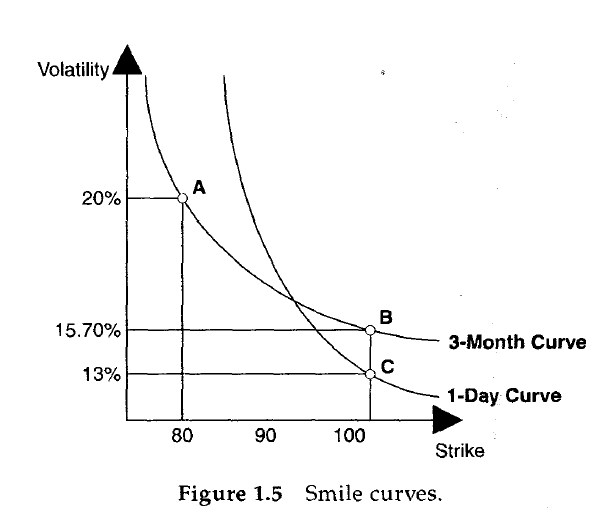

On page 28 of "Dynamic Hedging" by Nassim Taleb, he uses the following example to demonstrate the fact that a rising volatility curve could separate puts/calls for American options because the non-exercisable leg would follow the nominal maturity, whereas the exercisable one would have a shorter expected life. Looking at the second example below, could someone explain why the 3-month 80 American call would trade at 13% volatility (Point C)?