I'm thinking about how to select the $J$, and particularly, $K$ parameters for the Two Scale Realized Volatility estimation? I cannot find any reference for that in the original paper - there it says $K=cn^{\frac{2}{2}}$, but I couldn't find what exactly is $c$, $n$ is number of observations.

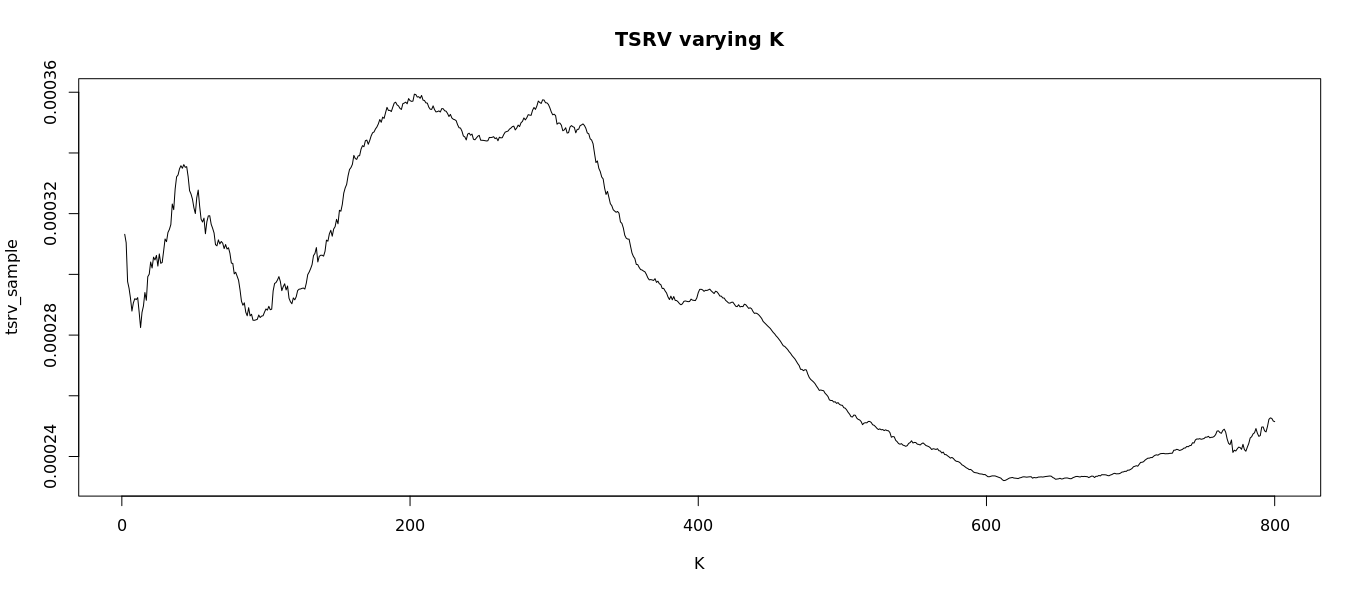

I've been playing around with the highfrequency package in R which offers a test set of of 8100 1-minute stock prices. If you estimate TSRV with rRTSCov, it seems that the estimation is quite sensitive to $K$.

My ultimate goal is to estimate 10 or 30-minute volatility with 10-second prices. How would I pick parameters for that? Is it large enough sample?

Many thanks for suggestions.