Assume a number of bonds with three constant variables, par value $par$, coupon value $C$ (paid annually), and interest rate $r$, and one changing variable, time to maturity $n$

First off, the relevant formulas:

The price $P$ of each bond, as you've already written it, is

$$ P=C*[\frac{1}{r}-\frac{1}{r}*\frac{1}{(1+r)^{n}}]+\frac{par}{(1+r)^{n}} $$

The duration $D$ of each bond is

$$ D = \sum_{t=1}^{n}{w_t*t} $$

where $w_t$ is

$$ w_t = \frac{C_t}{(1+r)^t}*\frac{1}{P} $$

The volatility $V$ (modified duration) of each bond is

$$ V = \frac{D}{(1+r)} $$

The modified duration $V$ gives an exact measure of the bond's exposure to interest rates. Thus the bond price sensitivity to interest rates is

$$ \frac{\Delta P}{P} = -V*\Delta r $$

Now if you put all these together it should easily follow that "the longer the bond the higher the sensitivity to interest rates".

First off, it's probably easy to see how $P$ relates to $n$. As $n$ goes up $P$ goes up as well. As $n$ gets bigger however the price increase rate drops and you eventually get closer and closer to $\frac{C}{r}$ (perpetuity formula). You do however constantly move up.

Similarly, as $n$ gets bigger, the bond duration $D$ increases as well. It also approaches a limit but it continuously increases.

By now you should probably see where I'm going with this. As $D$ gets bigger, $V$ gets bigger as well. As $V$ gets bigger the bond price sensitivity to interest rates goes up as well ($-V*\Delta r$ gets bigger for all $r$).

It follows then that as $n$ gets bigger (the bond becomes 'longer') the bond price sensitivity to rates goes up as well.

To see a numerical example as well have a look at the following charts (links point to imgur because I can't post more than 2 links or any pictures yet):

$C = 100, par = 1000, r = 0.05, \Delta r = 0.001$

$n$ on the x axis, price, duration, and bond price change on the y axes

$P(n)$, $D(n)$, and $\frac{\Delta P}{P}$ for $0.001$ increase in $r$

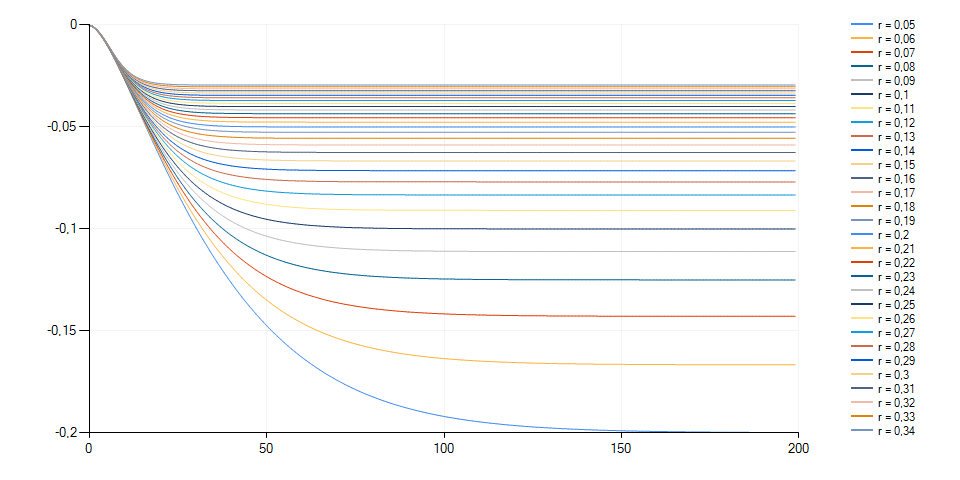

$\frac{\Delta P}{P}$ for $0.001$ increase in $r$ for multiple $r$ levels

{kind=link}

Ultimately I end up with a graph similar to yours but with no surprising results. There's no bond price change line curving up. All lines should eventually get closer and closer to a limit and then move to the right almost horizontally.

To wrap it up in terms of algebraic computations and thus address your second question we have the following:

$$ \lim_{n \to +\infty}P = \frac{C}{r} $$

$$ \lim_{n \to +\infty}D = 1+\frac{1}{r} $$

$$ \lim_{n \to +\infty}V = \frac{1}{r} $$

So to also answer your second question, yes, mathematically speaking the numbers confirm the answer to the first question, and if you increase the length of the bond up to infinity you can also calculate the relevant limits.

The numbers and charts used in the numerical example above confirm these formulas. The bond price approaches $C/r$ which in the above example is $100/0.05$, the bond duration approaches $21$ which is $1 + 1/0.05$, volatility approaches $20$ which is $1/0.05$, and the bond price sensitivity to interest rates approaches $-0.02$ which is $0.001*(-20)$