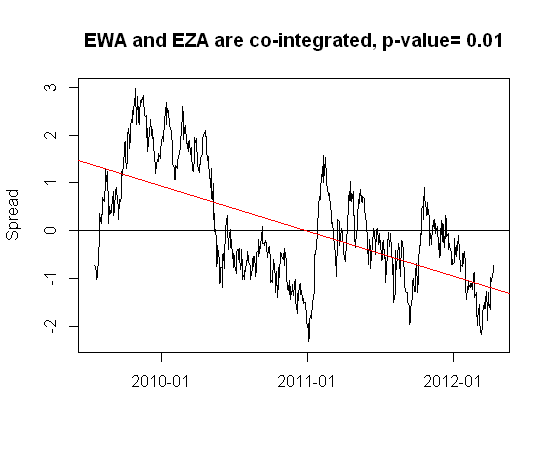

Below is a spread built with two ETFs that pass the cointegration test i.e. Adjusted Dickey Fuller, adfTest(type="nc") in R's fUnitRoots with a p-value < 0.01.

The red line is the trendline.

What test can I use to proove that: (1) both securities are cointegrated and (2) they are mean reversing and the mean is constantly 0 (i.e. stationary, not trended)?

Thanks