EDIT Since the weight generation process of my random portfolios seems to preffer too similar portfolio I changed the following function:

def random_portfolios(num_portfolios, mean_returns, cov_matrix, risk_free_rate):

results = np.zeros((3,num_portfolios))

weights_record = []

for i in range(num_portfolios):

weights = abs(np.random.randn(len(mean_returns)))

weights[weights<1] = 0

if sum(weights)==0:

print("sum=0")

indexes = np.unique(np.random.randint(0,10,3)).tolist()

weights[indexes] = abs(np.random.randn(len(indexes)))

weights /= np.sum(weights)

weights_record.append(weights)

portfolio_std_dev, portfolio_return = portfolio_annualised_performance(weights, mean_returns, cov_matrix)

results[0,i] = portfolio_std_dev

results[1,i] = portfolio_return

results[2,i] = (portfolio_return - risk_free_rate) / portfolio_std_dev

return results, weights_record

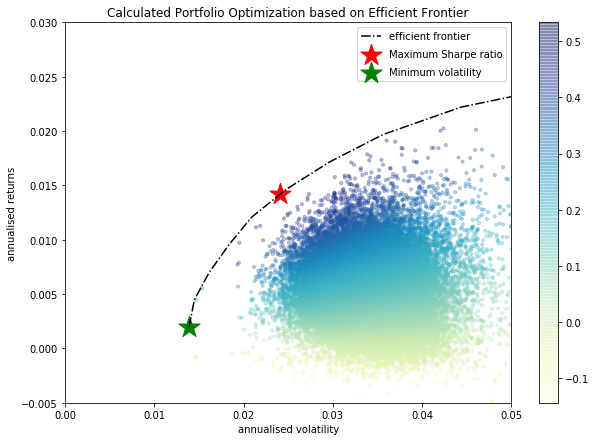

After doing so, the Portfolios are way better distributed:

So, can we then agree that the above code does what it should and I can continue from here?