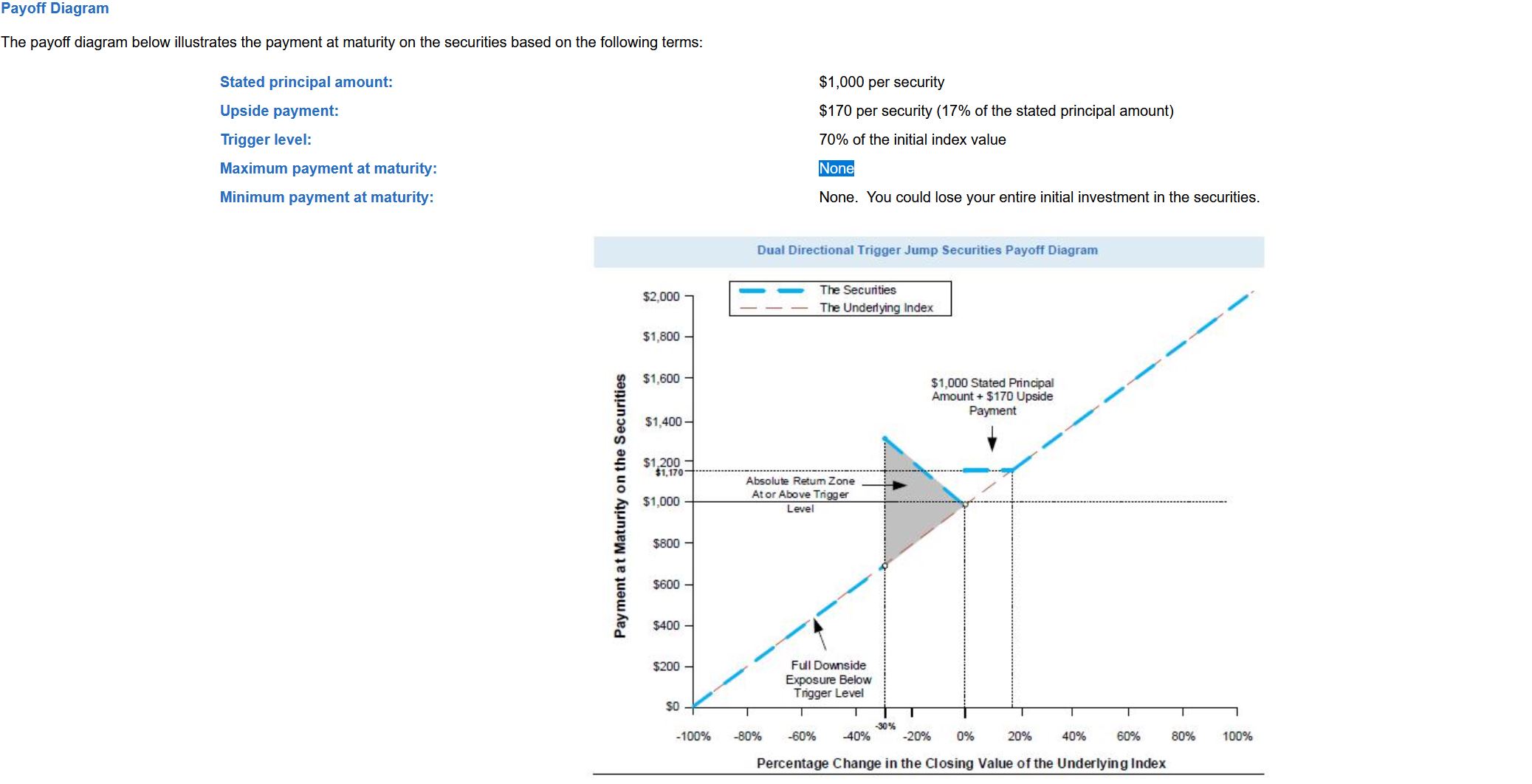

Well that’s the genius of marketing. But if you run the numbers, it’s not mispriced. As you point out, the holder receives no dividends and gets to take the risk of credit exposure to the issuer. I estimate the former is worth about 2% pa and the latter perhaps 1% pa , for a total of 3% over the 5yr term of this note, which is worth about 14% upfront or about usd140 per usd1000 bond. For this premium you get the payoffs that are in excess of the line. Eyeballing this I estimate the average payoff to be about usd225, given that you are in the performance zone (-30,+17). But the chances of being in this zone are quite small, I’d say about 30% using a back of the envelope calculation (one standard deviation after 5 years = annual vol *sqrt(5)= approx 20%*2.23= 44%. So the region covers about one standard deviation.) Well 30% of usd225 is less than usd140 so you can see there is plenty left for the bank.