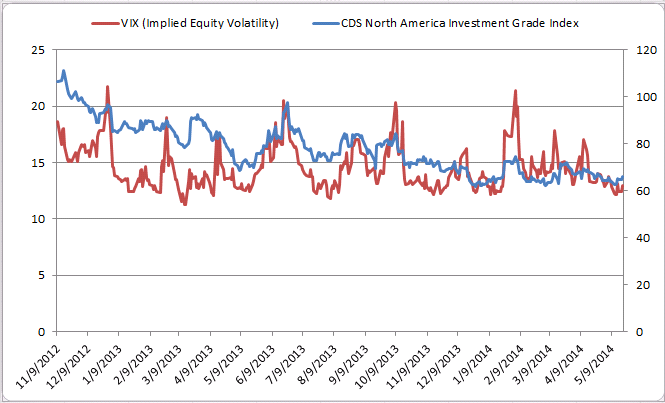

Why does CDS spreads track the implied volatility on equities? What is the fundamental relationship that would keep the two inline from deviating too far from each other?

My speculation: Could it be because CDS spreads are not necessarily “pure” compensation of default risk but also include spread volatility risk and that this spread volatility is a larger driver of the CDS spreads than default risk compensation and because it is highly correlated with equity volatility, that is the reason why bond insurance and stock insurance move in tandem. If it is the case, then CDS spreads are not “pure” default risk compensation, has anyone then built a way to filter out the spread volatility risk to arrive at the “Pure CDS Spread Default Compensation Risk ” for an issuer? Knowing the tight relationship between has anyone built an implied probability of default based on equity volatility for an obligor?

Would appreciate all your opinion on the topic.