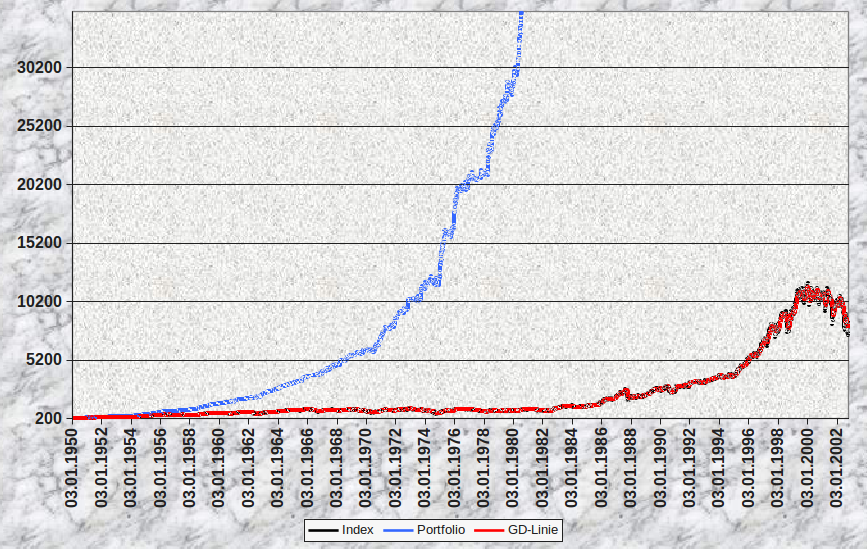

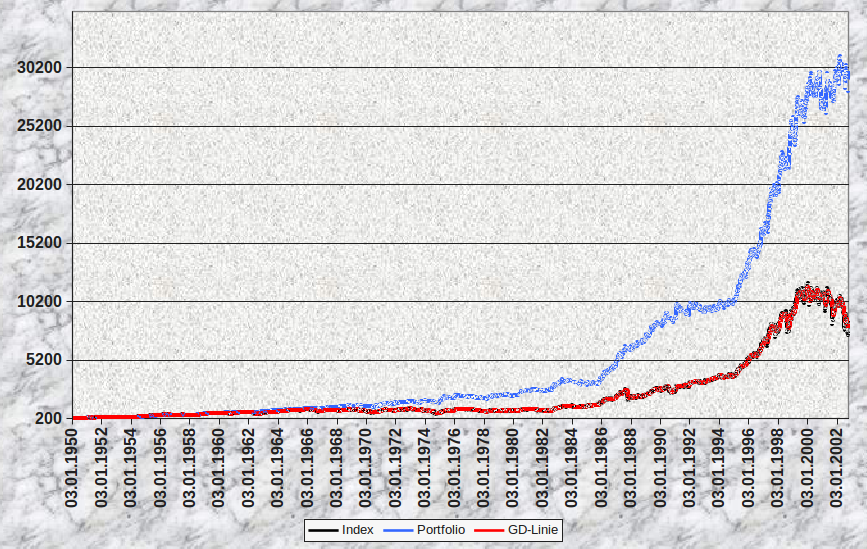

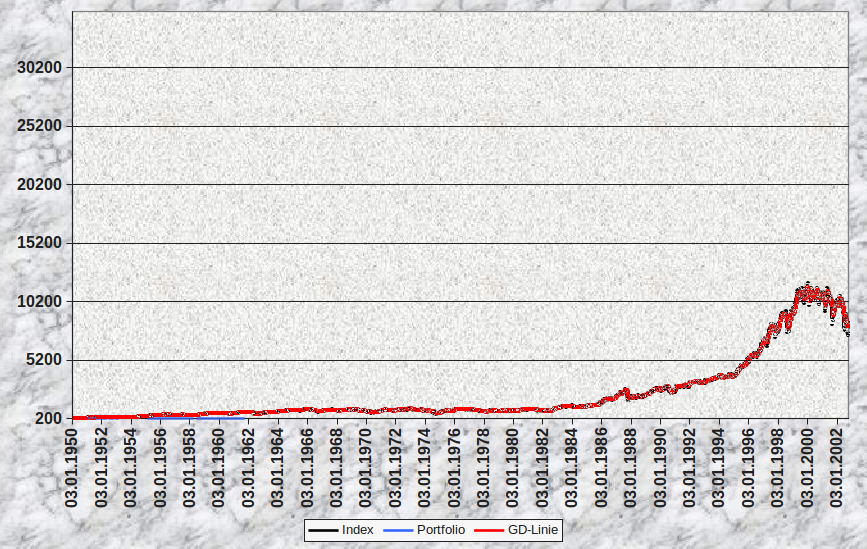

I apologize if this is way too basic a question, but I'm an absolute beginner to trading and am in the process of learning the fundamentals.

Currently I'm trying to model a (10-day) SMA backtest in Excel, where signals are generated due to crossovers between the closing prices and the 10-day SMA. I calculate the daily and cumulative returns based on closing prices for the asset, and then get the daily returns of the strategy by multiplying the daily asset returns by 1 (if long) or -1 (if short) (this method of getting strategy daily returns has been suggested in a couple of blogs that I'd referred to previously).

Finally I calculate the cumulative returns for the strategy. The problem is that the cumulative returns grow insanely large (I guess up to the order of $10^{15}$). I can't understand what I'm doing wrong - whether the formulae to compute returns are wrong or if the logic itself is incorrect.

I would be grateful if someone could check out the excel sheet (google drive link below) and let me know or at least give me a hint of where I'm making a mistake (or mistakes).