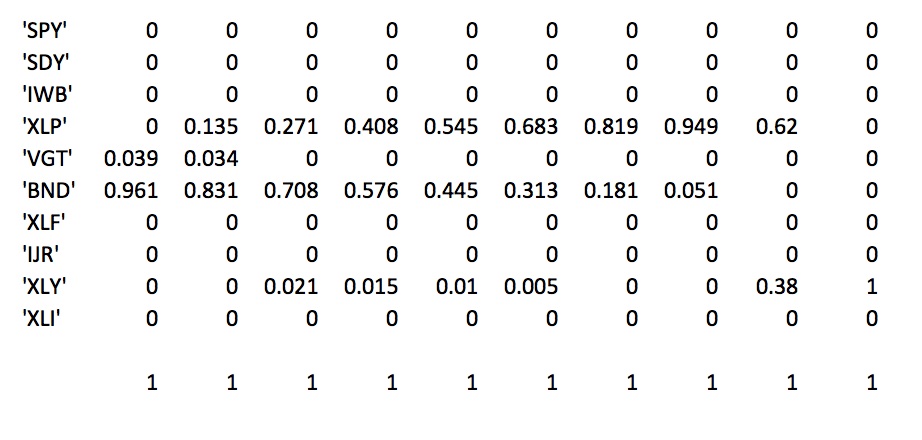

The long only minimum variance portfolio is either equal to the unconstrained minimum variance portfolio, which is usually dense, or it is guaranteed to be sparse - in the sense that there are only few nonzero coefficients. This is a consequence of the fact that the minimum is either achieved at the global minimum or at one of the corners of a convex polyhedron. A typical example for a dense long only portfolio result is from a diagonal covariance matrix.

At first this looks counterintiutive, as one intuitively equates low variance with low risk, and low risk and a sparse portfolio seems like a contradiction. But this method only looks at volatility - other aspects like default risk or so are ignored.

The usual trick is to increase the density of the resulting portfolio is to add a constant to the diagonal of the covariance matrix, thus making it more diagonal. The effect is to make the resulting portfolio more similar to the equal weight portfolio and thus less sparse.