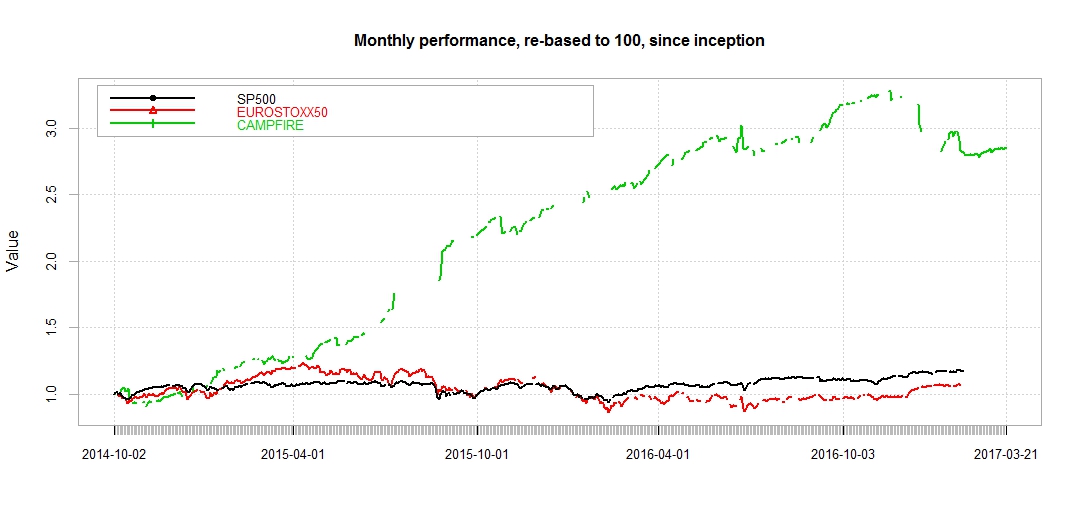

In R, with Performance analytics package, I am trying to chart multiple cumulative asset returns from an XTS object. The thing is that I miss some data from some asset returns so that the graph given from:

chart.CumReturns(XTS_DR_ALL[, c(1,2,5)], wealth.index = TRUE, main = "Monthly performance, re-based to 100, since inception", legend.loc="topleft", )

...plots non-continuous curves, which are not easy to visualize...

Can I do something to plot continuous lines for the asset returns of which I miss data? Best, Joe.