I found this power point and this paper to be an excellent source on this topic.

Here is a quote from the paper:

A square-root singularity for small traded volumes is highly

non-trivial, and certainly not accounted for in Kyle’s classical model

of impact [11], which predicts a linear impact ∆ ∝ Q. A concave impact

function is often thought of as a saturation of impact for large

volumes. We believe that the emphasis should rather be placed on the

anomalous high impact of small trades. Numerically, Eq. (1) means that

trading one hundredth of the daily volume moves the price by a tenth

of its daily volatility, which is indeed a huge amplification.

Mathematically, Eq. (1) implies that marginal impact diverges for

small volumes as $Q^{-1/2}$ , meaning that the susceptibility of the market

to trades of vanishing size is formally infinite. In most systems, the

response to a small perturbation is linear, i.e. small disturbances

lead to small effects. The breakdown of linear response often implies

that the system is at, or close to, a critical point, where very

special properties emerge, such as long-range memory or scale

invariant avalanches, that accompany this diverging susceptibility.

It goes on to say that besides being empirically robust (it appears to hold in a suprisingly wide number of settings), the square root law arises according to the authors from the very peculiar nature of the order book (the collection of all buy and sell orders) near the boundary between buying and selling. Closer to the "current price", the order book rapidly thins in density.

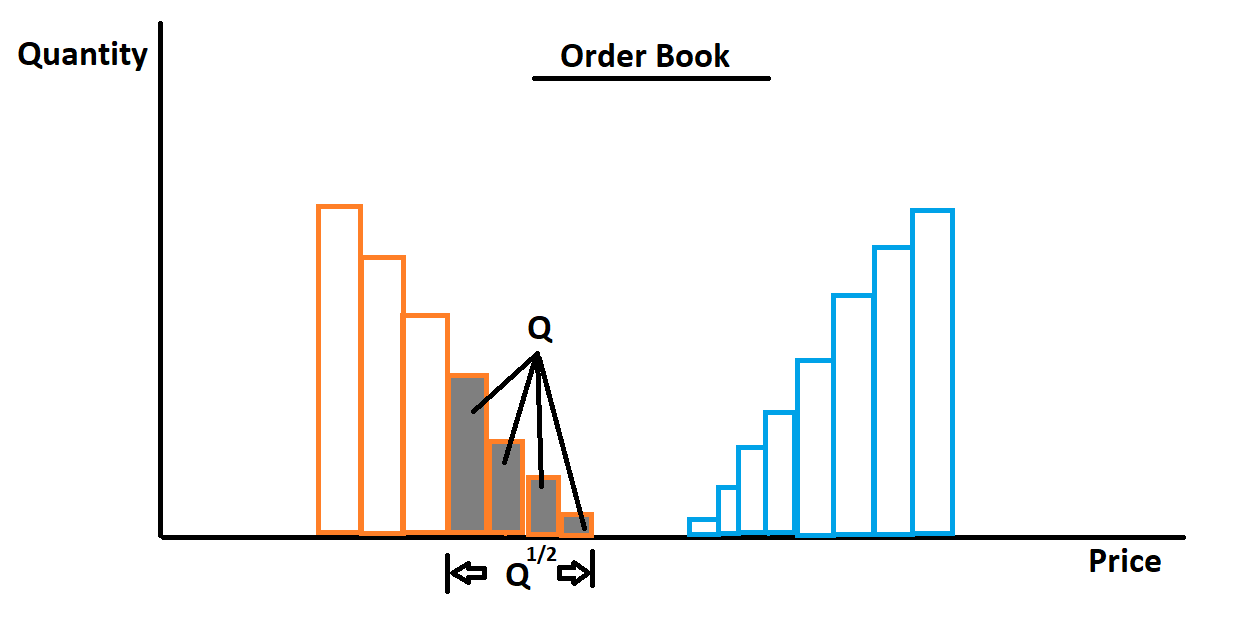

Indeed if this thinning in price-space of the order book is approximately linear, then the window in price space required to fill an order of dollar size Q will grow with the square root of Q (my own illustration):

Their model to explain this thinning supposes that orders undergo a diffusion process in price space (a diffusion associated with volatility), and therefore, the order book thins in density near the critical point where buy and sell orders meet each other and annihilate (execute).