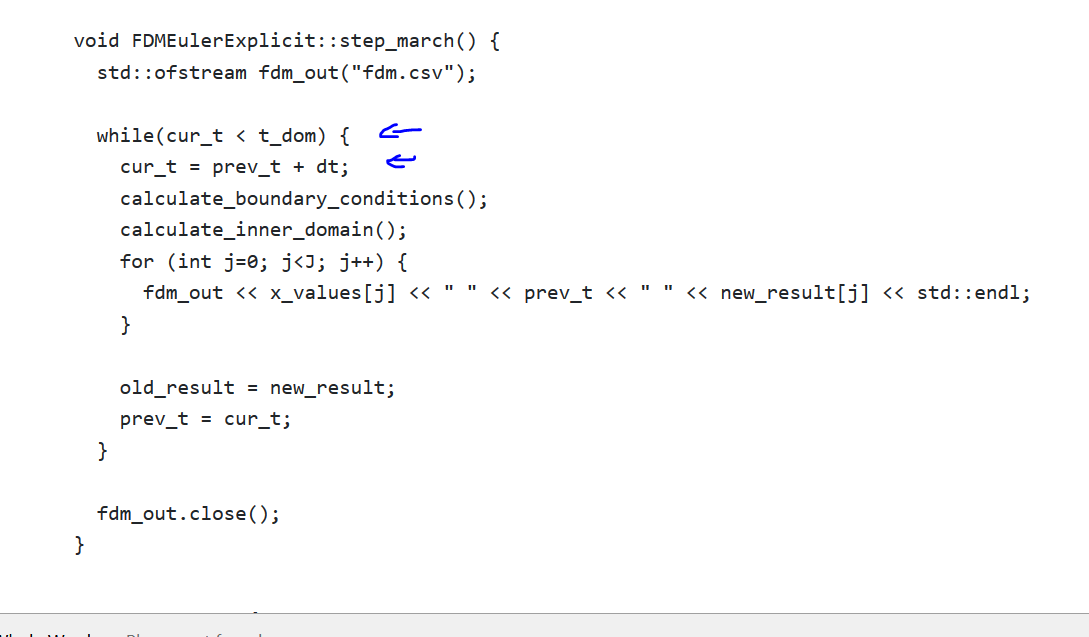

In finite differences for the black scholes method, you move backwards in time, since of course you know the prices at time $t = T$, and then you iterate until you get to time $t = 0$.

However, why then in this code does the time move forwards? Here, cur_t is current time, and as you can see, he iterates and each time moves cut_r forwards by dt.

Entire code can be found here: https://www.quantstart.com/articles/C-Explicit-Euler-Finite-Difference-Method-for-Black-Scholes

Is this a mistake in the code?