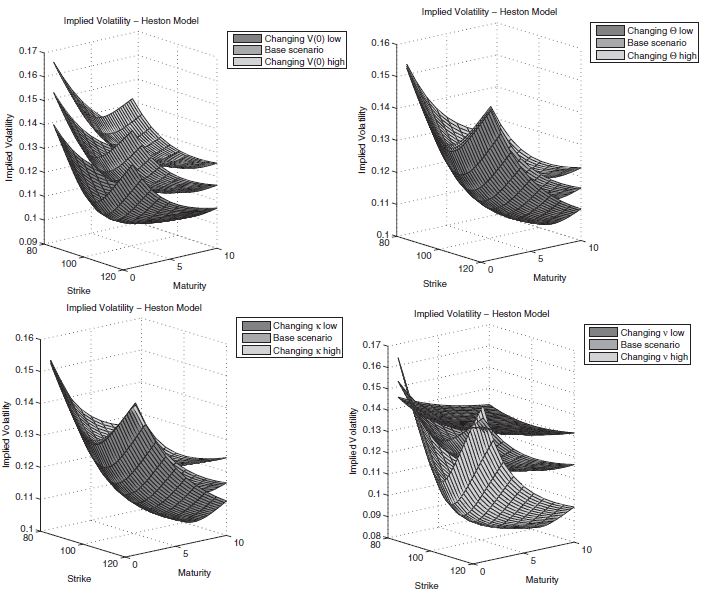

I was hoping someone could describe the economic/mathematical intuition behind the effect that the vol of vol parameter has on the volatility surface, in particular the slope to maturity. Take for instance, as in Kienitz and Wetterau (2012), the model as $$dS(t)=\mu S(t)dt+\sqrt{V(t)}S(t)dW_1(t)$$ $$dV(t)=\kappa(\Theta-V(t))dt+\nu\sqrt{V(t)}dW_2(t)$$ $$S(0)=S_0$$ $$V(0)=V_0$$ $$\langle\,dW_1,dW_2\rangle=\rho dt$$

The authors then supply the following vol surfaces after perturbing certain parameters:

All of these make sense to me accept the final chart showing the effects of perturbing the vol of vol, $\nu$. The more pronounced smiles at any given maturity are fine, I get those. I may be missing something obvious, but how does a higher vol of vol, all else equal, lead to declining option prices as we extend the maturity?