I think the fundamental misunderstanding you have is that you think that Cash Flows from Financing Activities includes interest payments. It does not. In only includes principal repayments. Cash Flows from Operating Activities does include interest payments. Look at any Income Statement + Cash Flow Statement on any 10-K from sec.gov and you'll see this to be true.

As Charlie Munger says, "I've never heard an intelligent cost of capital discussion".

Cost of capital can mean two things, and it's often not clear which definition people are using. Cost of capital can mean:

- how much it costs you to borrow money (e.g. 8% annualized interest rate to borrow \$1m with 10% outstanding principal repayment every year)

- the opportunity cost of deploying your capital into whatever you're calculating NPV for (e.g. 9% historical nominal return from the S&P 500)

The discount rate matters for the second. It doesn't matter for the first.

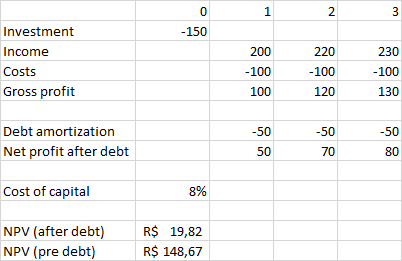

Now, all that being said, to calculate the NPV of an investment, all that matters is how much cash you outlay initially and how much you're getting back at each period of time. Therefore, you are correct that debt repayment, in terms of both interest and principal should be taken into account when calculating NPV.

Let's take two examples. Let's say you're thinking about buying a private business for \$1m dollars that has \$1m book value (assets - liabilities, or in other words, equity) and returns 10% free cash flow every year for five years after which we liquidate the business and sell the \$1m of assets net of liabilities. For sake of example, the only other investment possibility you have is to invest in the S&P 500, which will return you 9% guaranteed (again, for sake of example). Because this 9% is your opportunity cost, it will be used as the discount factor.

We'll first do the calculations using \$1m equity (money you own), then we'll do it with a mix of equity and debt with a specific cost of capital, where the cost of capital definition is the first one from above.

Example 1 (Use \$1m equity to buy business):

$\text{NPV} = \\\$100,000 / 1.09 + \\\$100,000 / 1.09 ^ 2 + ... + \\\$100,000 / 1.09 ^ 5 + \\\$1,000,000 / 1.09 ^ 5 - \\\$1,000,000$

NPV = \$38,896.51

Example 2 (Use \$500k equity to buy business and \$500k debt at 5%):

The interest payments are as follows, which I plugged into: https://www.creditkarma.com/calculators/amortization/

Year 1: \$22,950

Year 2: \$18,331

Year 3: \$13,476

Year 4: \$8,372

Year 5: \$3,008

Cumulative principal you've paid off every year is:

Year 1: \$90,278

Year 2: \$185,174

Year 3: \$284,926

Year 4: \$389,780

Year 5: \$500,000

$\text{NPV} = (\\\$100,000 - \\\$22,958 - \\\$90,278) / 1.09 + (\\\$100,000 - \\\$12,331 - \\\$94,896) / 1.09^2 + (\\\$100,000 - \\\$3,008 - \\\$99,752)/ 1.09^3 + (\\\$100,000 - \\\$13,476 - \\\$$104,854)/ 1.09^4 + (\$100,000 - \$8,372 - \$110,220)/ 1.09^5 + \$1,000,000/ 1.09^5 - \$500,000

NPV = \$104505.26

Notice that the cost of debt here has nothing to do with the discount factor. The opportunity cost of capital has everything to do with it. The cost of capital (first definition) is handled by the interest and principal payments on the numerator. Also notice that the NPV of the second calculation is bigger because your return on equity was higher (you only put up \$500,000 instead of \$1m and you were able to borrow at 5% while getting a 10% return on the money, thus covering your cost of capital (first definition)).

PS: this link I recently found was enlightening and uses a more intuitive answer if you're not inclined towards math: https://www.managementstudyguide.com/effect-on-free-cash-flow.htm