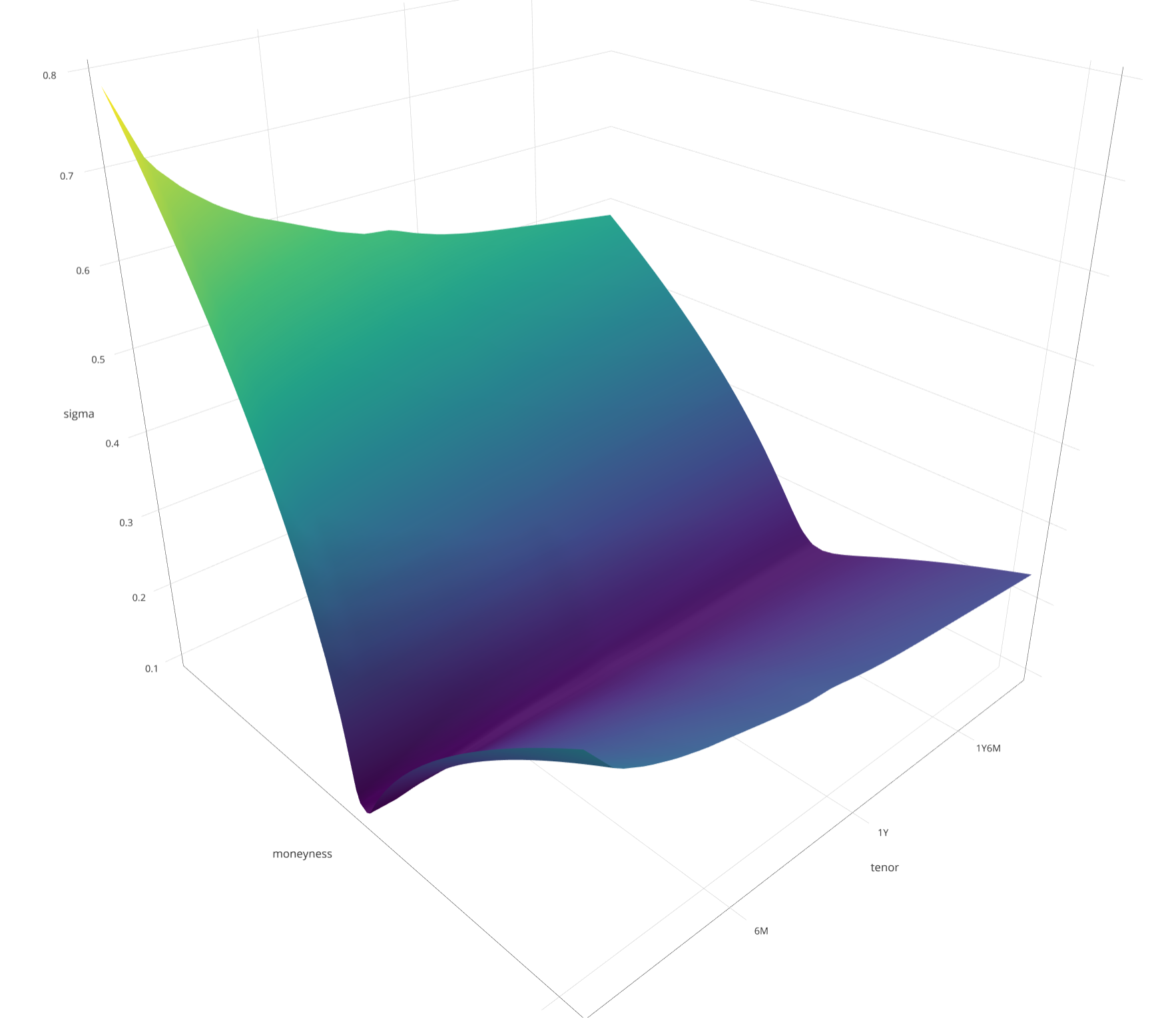

I would like to normalise options, to being able to compare it. Make price of underlying symbol = 1, have same tenors, and same step for the strike price.

1) Use 1 as stock_price and scale strike_price accordingly, easy to do.

2) Use same step for strike prices. Different options have different step for strike prices, for one option step could be 10% (so strike prices for CALL will be 110%, 120% etc), for another option step could be 15% (strike prices will be 115%, 130%, etc). I would like to re-scale it and use same step for all options. The problem - you need interpolate strike_prices to get those normalised values.

3) Normalise expiry date or tenors. Again different options have different expiration dates, I would like to normalise it to say 1month, 6month, 1year. Again strike_prices needs to be somehow interpolated to get those values. Any good approach to interpolate strike_prices over dates?

Are there any conventional, standard methods to do that? What functions to use for interpolation - polynomial, exponential? How to fit it, with regression?