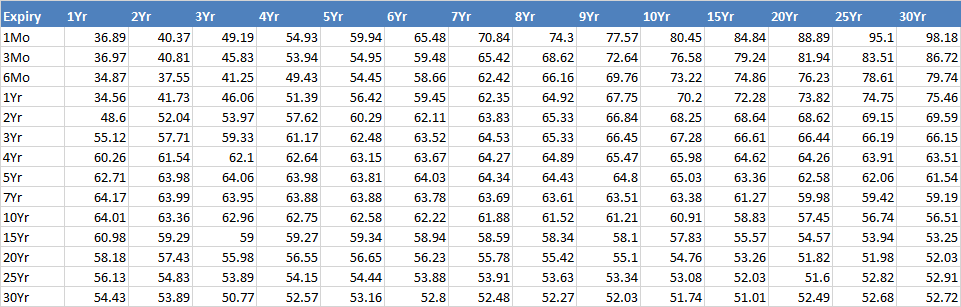

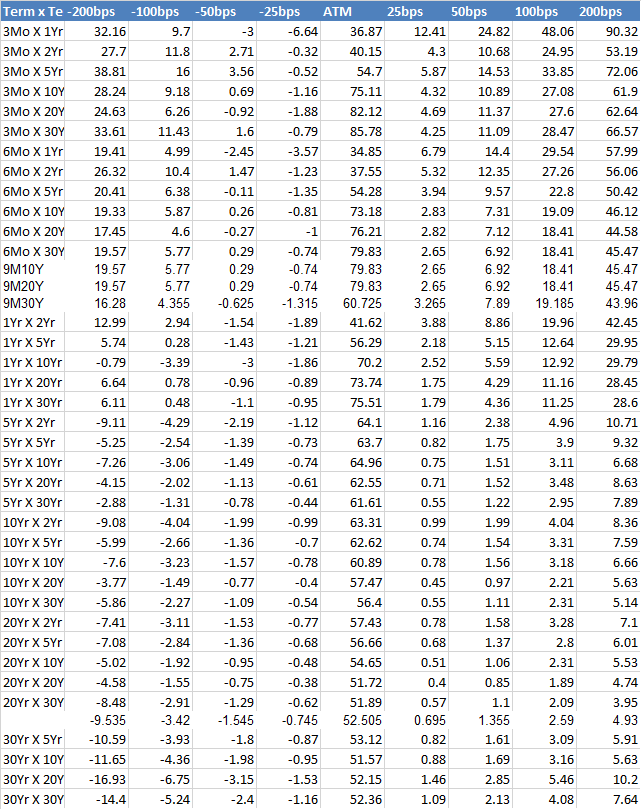

How can I build a good vol surface using QuantlibXl? My goal is to price a swaption 5 year with option maturity 1Y1M.

The data are:

How can I build a good vol surface using QuantlibXl? My goal is to price a swaption 5 year with option maturity 1Y1M.

The data are:

The procedure is to build an ATM swaption vol matrix using qlSwaptionVTSMatrix. Then extend that to a swaption vol cube to add the skew data using qlSwaptionVolCube2. Then you can feed this volcube to a swaption pricer. You can find arguments for these functions here: https://www.quantlib.org/quantlibxl/allfunctions.html. Note that QuantlibXL limits swaption valuation to ShiftedLognormal vols, so you cannot use a normal vols for instance.