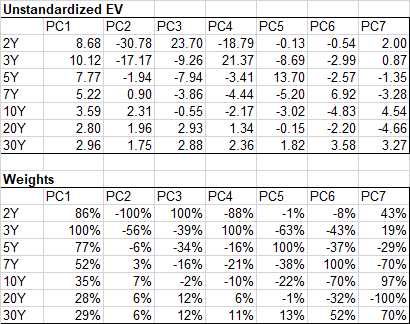

I have a daily US swaps data here for 2020 https://easyupload.io/yh4rnd . I have run PCA on standardized data and got PCA matrix (and basic statistics):

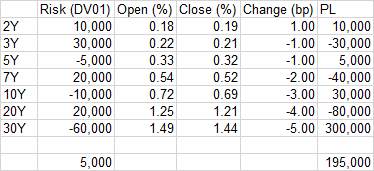

I also have such hypothetical portfolio that in this example is making +$195k.

Question: How do I attribute this P&L to each principal component, such that the total P&L number equals +$195k?

Working through suggestion by Dimitri:

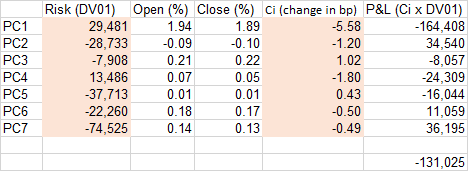

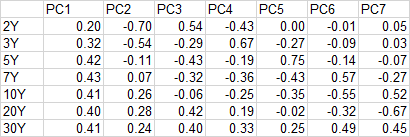

Assuming we cannot fully reprice portfolio using a perturbed interest rate curve, so will go with DV01s. To calculate ci for each PCi I converted PCA on standardized data back to unstandardized and calculated weights below for each tenor x PC, then for each PCi I calculated Open and Close in % (eg PC1 opened at 1.94 and closed at 1.89) with c1 euqal to -5.58bp (I checked, each PCi is orthogonal). I then used the same weights to convert original risk from hypothetical book into PCi. I then multiply ciPCi x δ to get P&L. But it doesn't seem to match up, which step am I getting wrong?