This question is about something observed hands on data that makes me a little confused.

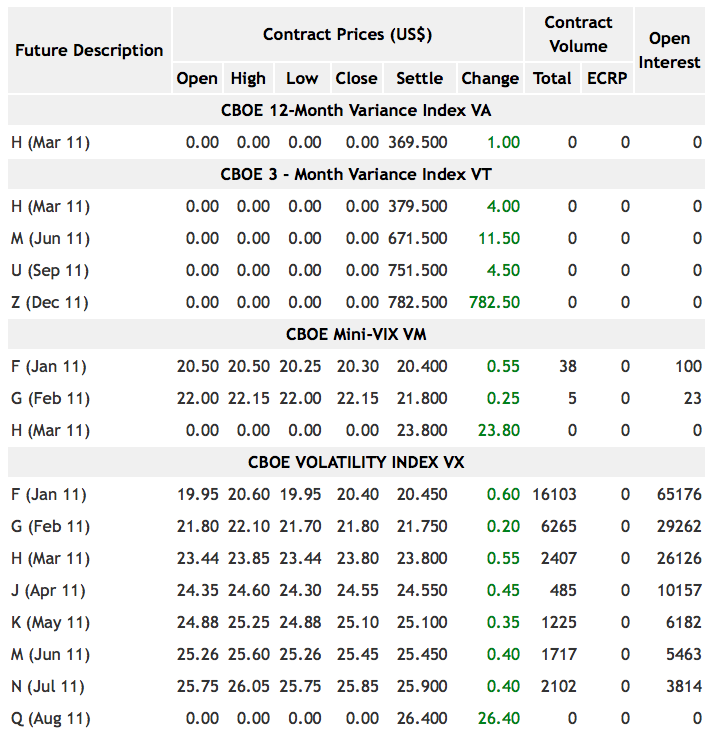

Consider the term structure of futures on VIX of Monday, December 27, 2010. You can find it at the CFE market statistics webpage. This day is the first day in which the recently issued contract Q (Aug 11) - introduced on Tuesday, December 07, 2010 - began being priced, with settle price: 26.4 US$; but at the same time, closing day Volumes and Open Interests still are null...

This day is the first day in which the recently issued contract Q (Aug 11) - introduced on Tuesday, December 07, 2010 - began being priced, with settle price: 26.4 US$; but at the same time, closing day Volumes and Open Interests still are null...

This makes me a bit confused. Is it completely normal? I guess so, but don't know why. Thanks to anybody that may clarify me on this point.