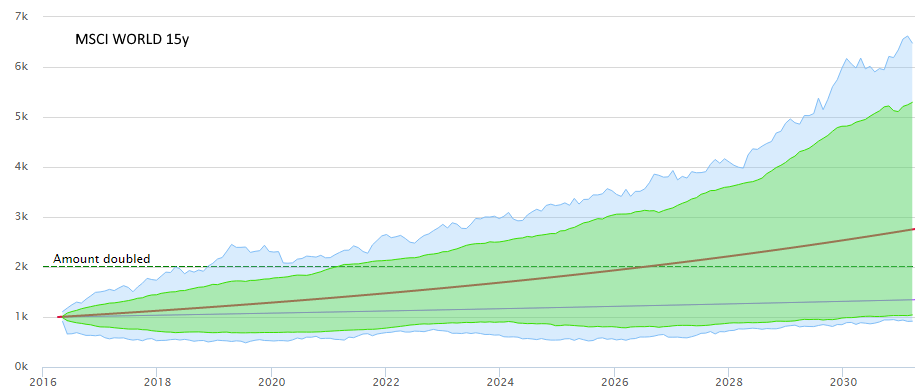

When looking at historical data (index or stock), one can find all 1-day differences/movements, all 2-day, all 3-day etc and graph the extremes of each of these. This gives two line graphs forming a channel/fan showing the historically maximum price fluctuations for being in this stock for 1 day, 2 days etc. It is quite an instructive graph showing how risk tends to narrow over time. See example where MSCI World (15 years of monthly closes) are used to show the historical extreme outliers (blue) and also the 90% band (green - which one might think of as a historical confidence interval of sorts). The two lines are just 2% and 7% interest rates for comparison. I thought of this myself, but I have surely not found something new. So what is this graph or method called, where can I read more about it and how can I approach quantifying what it shows?

-

$\begingroup$ The title of the question is a bit misleading ... $\endgroup$– Richi WaCommented Apr 6, 2016 at 5:38

2 Answers

Sounds a little bit similar to variance ratio - the seminal paper of which was Lo, MacKinlay 1988, however that deals with variance, not differences of extrema.

That you find "risk" narrows over time is odd, given that $Var[x + y] = Var[x] + Var[y]$ for independent variables $x \& y$, and one could look at days as being independent, and similarly distributed (not identical as mean and variance can change) for typical stock time series (at least that is the random walk hypothesis). However, if you were, for example, dealing with a time series that exhibited mean reversion or auto-correlation, this could affect it slightly.

I think it might also depend on your methodology - am not entirely sure what "graph the extremes of each of these" means. It seems to me that the min and max should be typically moving apart from each other, if slowly. If dividing the differences by the number of days, then yes it will surely converge, as the probability of having found a (relatively random) series with n positive (or negative) days as large (or small) as the max (or min) move becomes negligible quite quickly. ;-)

-- Edit -- It looks like returns - is it? (percentage or log?) I think perhaps you are graphing the min/max of the n-day returns distribution? If that's a correct assumption it seems fair to me to say it's the graph of the best or worst one could have done over each holding period, for the entire data set (the time axis of 2016-2031 is presumably an extrapolation of $1000 from now?)

How does it compare to what might have happened - or what was likely? Good question. On the basis of some (only 500) Monte Carlo simulations, presuming lognormal returns, similar drift to the stock, and constant volatility similar to the historical, I did this for AAPL over a 15 year period for 1-500 day returns.

Mins & Maxes shows the min & max values that the monte-carlo sims took, Averages shows the average values that the monte-carlo took. One can see that AAPL was within the range of Monte-Carlo sim (min/max), but a little more dispersed than the 'average'. What conclusions can one draw? I think it's a reasonably simple way to show what was described above - the best or worst one would expect to do over a period? Beyond that I don't know. If it were significantly different from monte-carlo, one might wonder, but then it becomes a statistical question about the likelihood of it being within a certain range.

-

$\begingroup$ I really appreciate your input. I have edited the question to show an example. The word risk is (still) used imprecisely. The graph (data from msci world) shows that the historical worst ever is relatively constant over time, perhaps having a slight upwards trend over time. I think this graph can be used to say (although our future could be the worst or best ever, so could go outside of historical data): 1) you risk losing half your assets 2) on average the nominal return is 7% (red line), 3) it will take more (and might be a lot more) than two years for your money to double.Input appreciated. $\endgroup$ Commented Apr 5, 2016 at 16:10

-

$\begingroup$ Ok updating my answer a little in light of your response... $\endgroup$ Commented Apr 6, 2016 at 1:30

-

$\begingroup$ It is indeed the n-day returns distribution. Returns calculated as (Xn-X0)/X0 where n and 0 moves along the dataset. The time axis is extrapolation from today. Sorry for my convoluted way of describing it originally. A short follow-up, if I may, could you point me in the direction of academic/formal backing of your statement (which is my intuitive understanding as well): "[..] it seems fair to me to say it's the graph of the best or worst one could have done over each holding period"? $\endgroup$ Commented Apr 6, 2016 at 13:13

-

$\begingroup$ Nice book on asset price dynamics by Stephen Taylor. The statement is simply observed from the data. Future asset price likelihoods forms the basis of option pricing, I'm sure you're aware. This book is well known Options, Futures and Other Derivatives $\endgroup$ Commented Apr 6, 2016 at 18:05

If you look at longer time returns (monthly or weekly as compared to daily) then these can be seen as the sum of daily (log-)returns: $$ r^w = \sum r_1^d + \cdots r_5^d. $$ It is in general not true that the $r_i$ are iid because they are not independent. If they were then $r_i^2$ would be iid too and we know that volatility clusters. Even without independence we see that variance roughly scales with time.

The thing that you might be seeing here is aggregational Gaussianity (see e.g. here in a paper by Rogers and Zhang. This means that increasing the time scale returns look more and more Gaussian. This implies that excess kurtosis gets smaller and skewness too. This leads too a distribution with less "suprises" and in this definition less risk.

-

$\begingroup$ Thank you for the input. It gave me stuff to read up on. Your last paragraph in particular. $\endgroup$ Commented Apr 6, 2016 at 13:17

-

$\begingroup$ @Richard Hardy, do you suggest we wouldn't observe volatility clustering with independent returns. Think Heston for instance (or any sv model). Periodic returns are independent from each other (driven by brownian increments), but their variance changes (spot/vol correlation), hence volatility clustering? $\endgroup$ Commented Apr 6, 2016 at 18:04

-

$\begingroup$ Hi, I am not Richard Hardy, my username ist just Richard. No, I would have to think a bit more about Heston here. But we speak of realized returns - right? So not risk neutral, just statistical. If their square shows autocorrelation, then they can not be independent. The square is related to volatility (as a formula and in intuition, if you think that sign does not matter but size). If returns were normal then correlation zero and independence are equivalent. For example a multivariate t-distributuion can have correlation zero but dependence. $\endgroup$– Richi WaCommented Apr 7, 2016 at 7:50

-

$\begingroup$ To see that returns can have correlation zero but be dependent think of $X,Y,Z>0$ independent, then $X/Z$ and $X/Y$ are uncorrelated but not independent as both are scaled by $Z$. $\endgroup$– Richi WaCommented Apr 7, 2016 at 7:51

-

1$\begingroup$ Hi and sorry @Richard. I agree with your last point of course (zero correlation = independence only for elliptic distributions, though I don't get the example)... but not entirely with the rest. First, risk-neutrality has nothing to do here, Heston is simply a diffusion model, it can be defined under P or under Q, that wouldn't change its 'global' statistical properties. Essentially, my point was you claim periodic returns are not iid because not independent, and I meant to point out that they can be not iid because not identically distributed either (heteroskedasticity). $\endgroup$ Commented Apr 9, 2016 at 9:12