http://www.volcube.com/resources/options-articles/gamma-hedging-trading-strategies-part-i/

I would like to have proven to me the above formula, mostly because I don't quite understand it. The formula is an approximation of the profit from gamma trading/gamma hedging, $$0.5 \Gamma (\Delta S)^2$$ So, my questions are, how to prove that, and secondly, what does it mean exactly by "profit"?

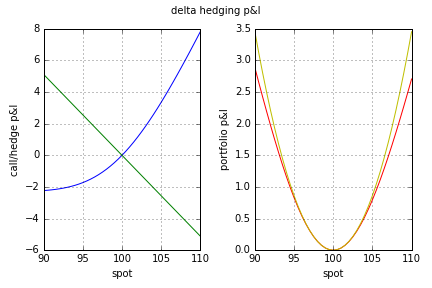

Example:

Today, an ATM 1-year 25 % volatility call is bought for 10, and we short $\Delta = 0.5$ in the underlying, which is worth 100. So working that out, we get portfolio value $\Pi = 10 - 50 = -40$, our portfolio value.

Some time later, the spot goes up to 105. The call goes up in value, from 10 to 13.

Currently we have shorted $0.5$ of the underlying, so we owe $0.5 \cdot 105 = 52.5$, so we have $\Pi = -39.5$.

So profit is 0.5.

Then we perform our re-hedge: if delta moved from 0.5 to 0.6, then we need to short 0.1 of the underlying. So, we add $-10.5$ to $\Pi$, i.e, $\Pi = -50$.

Where does the formula from above come into the picture here?