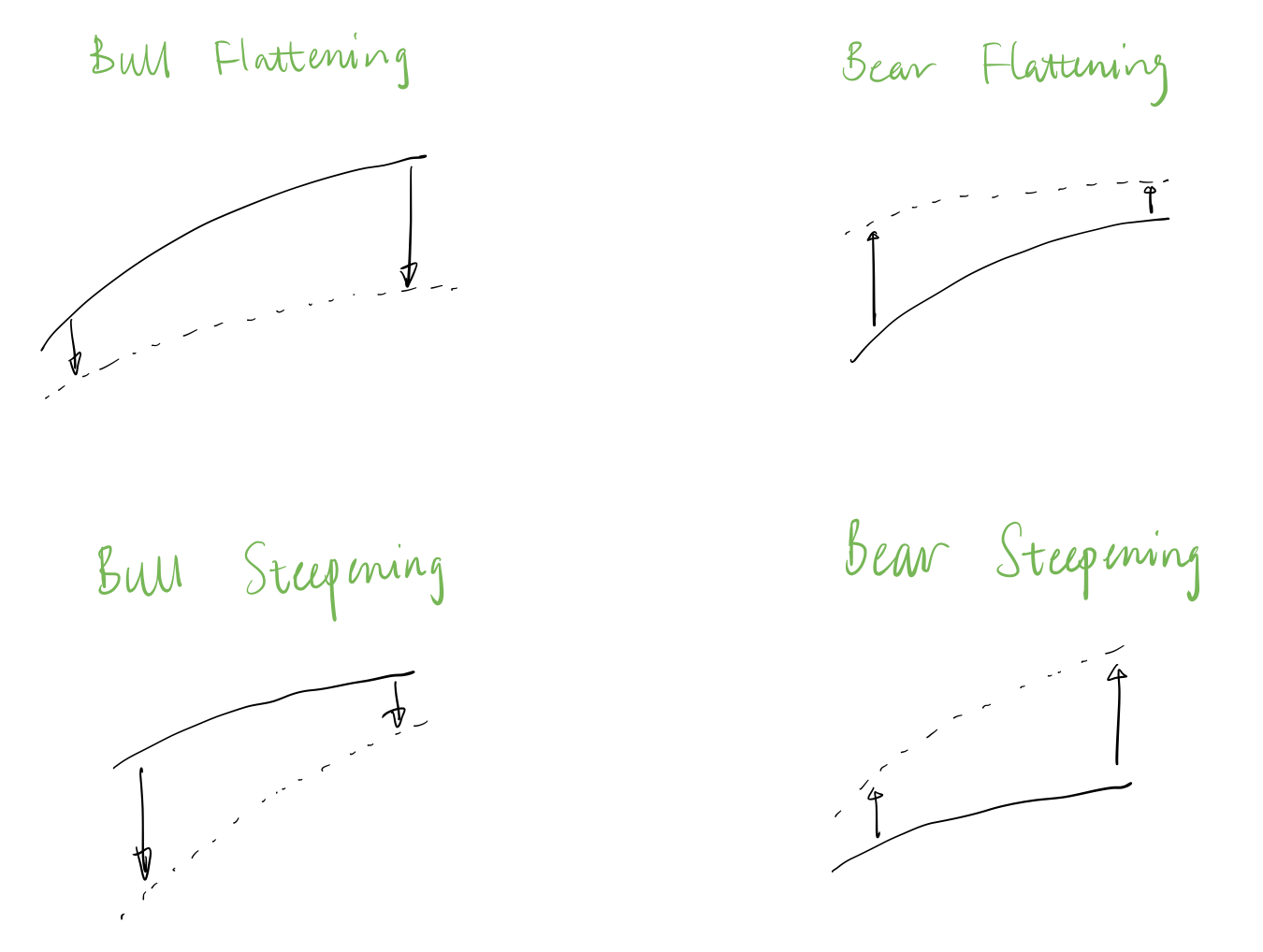

Please refer to the picture below for what each trade is betting on.

As an example, in a bull flattening trade, you're betting that rates will decline AND the yield curve will flatten. The flattening aspect can be easily expressed by buying a long-term bond, while simultaneously shorting a shorter-term bond. If you do NOT structure the two legs to be DV01 neutral, but with a residual long duration exposure, you'd have a bull flattener going on (in practice, this is rarely done). To more precisely express a "bull flattening" view, you need to venture into interest rate options. For example, buying long-rate receivers while selling short-rate receivers would accomplish the goal; this structure is known as a conditional bull steepener.

Other trades can be structured analogously.