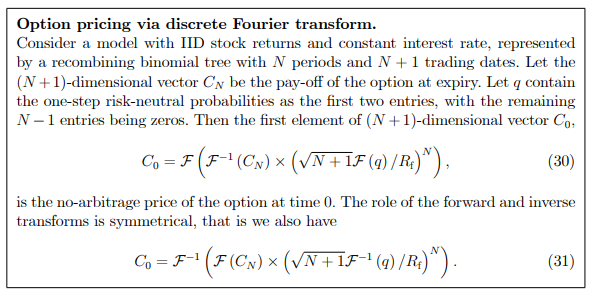

I am trying to implement the pricing formula for a European (call) option given in Ales Cerny's paper "Introduction to Fast Fourier Transform in Finance" (paper can be found here), as follows:

My python code below does not return the correct answer, and in particular if I significantly increase the number of steps then I get a much larger answer. Where have I gone wrong?

import numpy as np

from numpy.fft import fft, ifft

def price_vanilla_option(s: float,

k: float,

r: float,

ro: float,

t: float) -> float:

"""

price vanilla option using Fast Fourier Transform

"""

steps = 1023 # 2^n - 1 for efficient fft

d_t = t / steps

discount = 1/(1 + r * d_t)

# use CRR probabilities

u = np.exp(ro * np.sqrt(d_t))

d = np.exp(-ro * np.sqrt(d_t))

p = (np.exp(r * d_t) - d)/(u - d)

# set up terminal vector and prob vector

c_n = np.zeros(steps + 1)

c_n[0] = s * (d ** steps)

for i in range(1, steps + 1):

c_n[i] = c_n[i - 1] * u / d

c_n = np.maximum(c_n - k, 0)

p_vec = np.pad([p, 1 - p], (0, steps - 1))

# fast fourier transform

c_0 = fft(ifft(c_n) * np.power(fft(p_vec) * discount, steps))

return np.real(c_0[0])