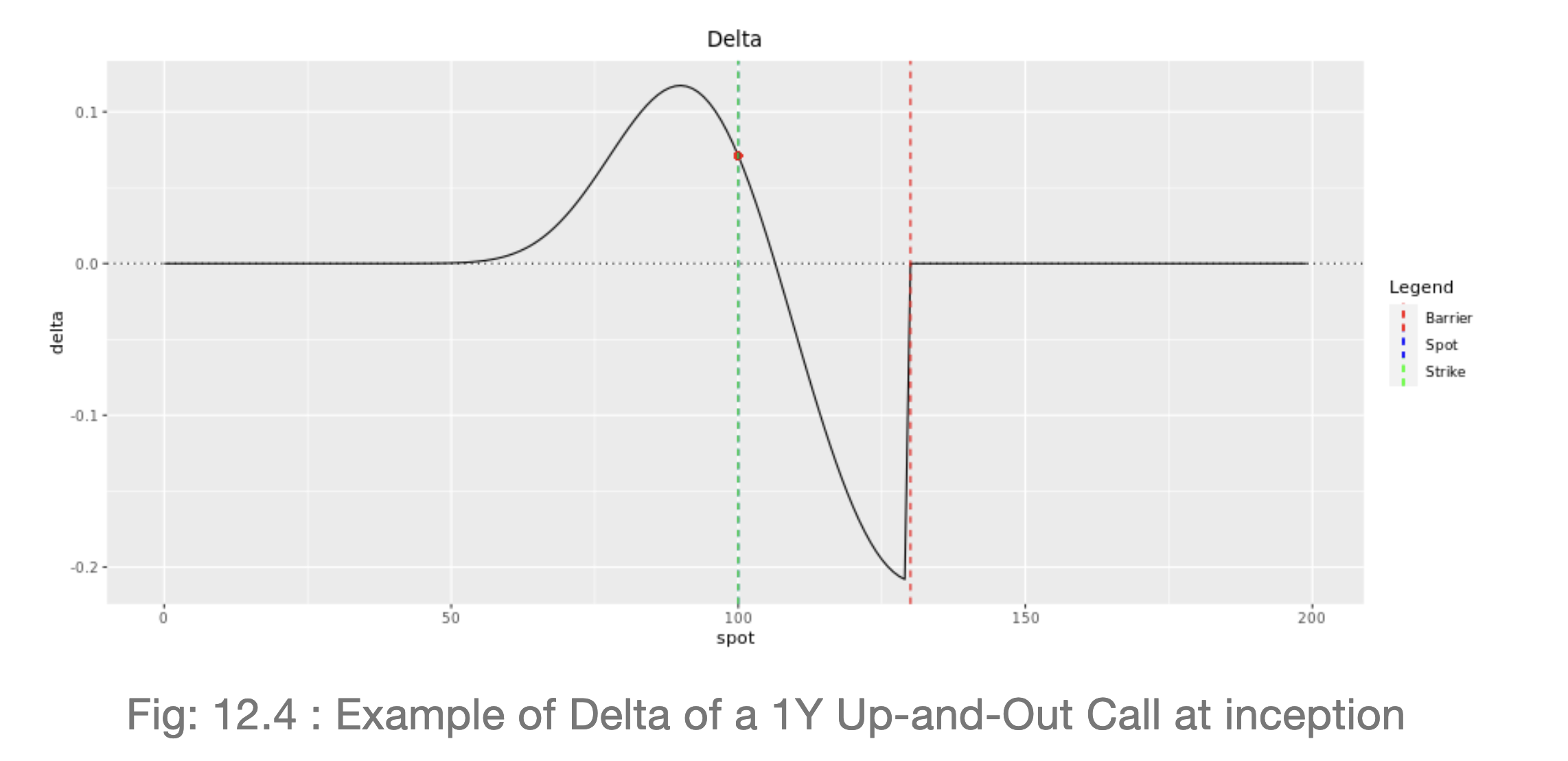

For Up And Out options, is there an intuition as to why delta becomes negative as spot approaches the barrier. Thinking in terms of replicating portfoliio I would have assumed delta is always non-negative (since there is positive (even if very small) probability of ending up below the barrier at T) approaching zero close to the barrier since there will be nothing to hedge once the barrier is crossed

I.e if you short an up and down barrier option why you need to short an option when close to barrier?

Picture from here