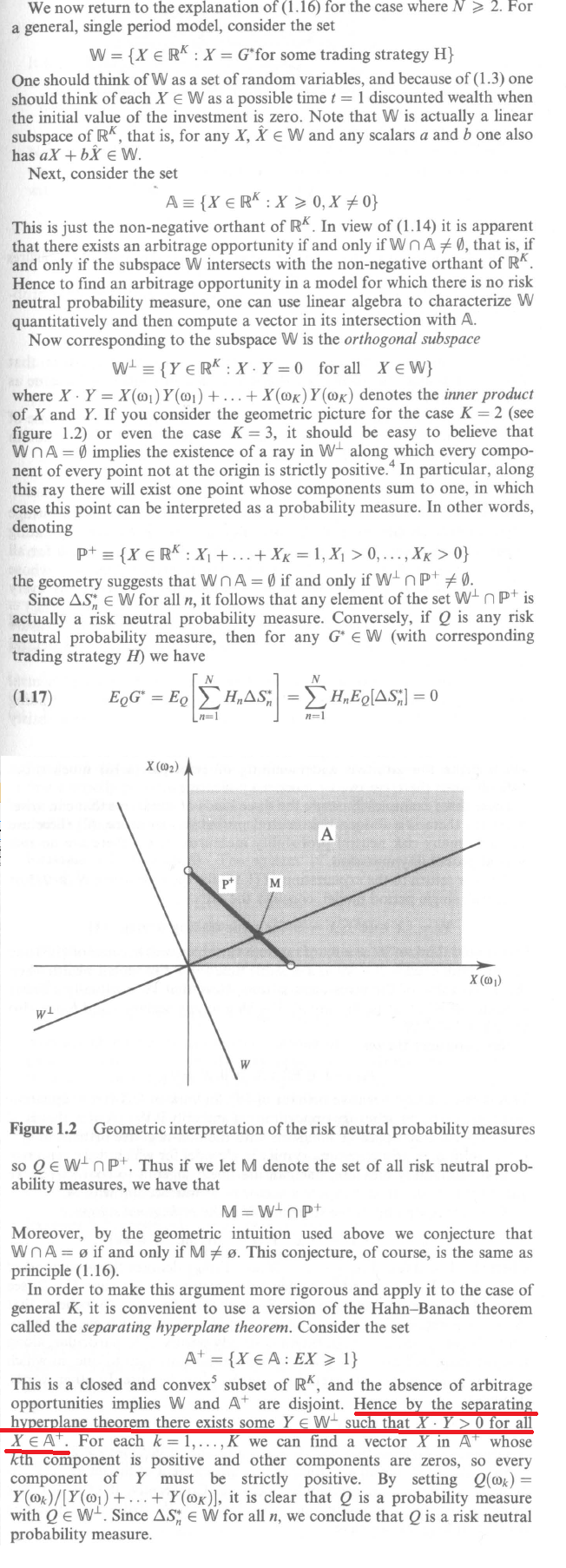

This is from Pliskas book in mathematical finance. I do not know what was best to write the question so I included the pages from the book. He has not written what form of the separating hyperplane theorem he uses, and why this follows. If someone understands it, could you please explain it? I have outlined in red the sentence I do not understand.

They refer to 1.3 which is: $V_t^*=V_t^*/B_t$, $t=0,1$

and 1.16: There are no arbitrage oppurtunities if and only if there exists a risk neutral probability measre on Q.

He also uses a single period model.