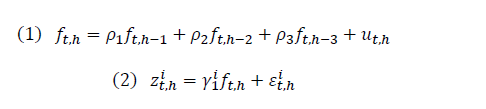

Is it possible to the extract the latent factor f from the following equations using kalman smoothing?

f is the unobserved state value while z is observed series.

From the literature i could read on web mostly the variable in state equation is a function of its previous one lag however here its a function of the last three lags.

Please, can you suggest some literature to understand the computation part and also would like to know which packages in R can be useful to implement this problem in particular

Link to original paper, refer to page 6