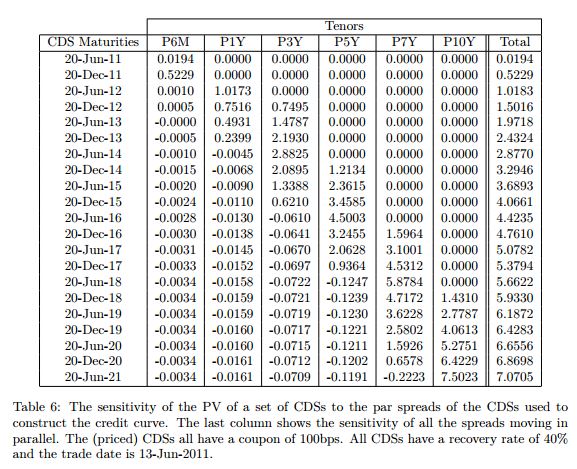

From page 27, Table 6:

Why are sensitivities of CDS slightly negative before the maturity of the CDS?

I do not get the intuition: if I am long a 5-year CDS, the spreads <5y increase, and the 5y spread remains constant, according to the table above I am loosing money because of the negative signs of the sensitivity. How is this possible?