I wouldn't put too much faith in IBES forecasts. You may remember this situation:

http://papers.ssrn.com/sol3/papers.cfm?abstract_id=889322

(In case the above link doesn't work, Google "Rewriting History Alexander Ljungqvist").

You'll find lots of excuses for worthless forecasts:

http://www.princeton.edu/~hhong/rje-analyst.pdf

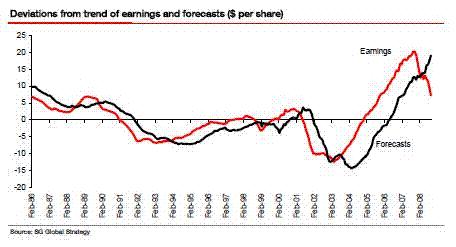

Below is a graph that I saved from some study. As I recall, their point was that analyst forecasts are typically nothing more than slightly modified naive forecasts (i.e. next year's earnings will be about the same as this year's earnings....and this was for analyst forecasts of S&P500 earnings). I'll post a reference if I can find it again.

The bottom line is, you're better off if you ignore analysts. From your own models you'll find that forecasting earnings for individual companies is a crap shoot. And, by far, the easiest earnings sequence to forecast is for the S&P500. However, that's by no means easy. Structural shifts happen without warning and model inputs that were useful for decades can easily drift into bizarre territory.

As far as your questions go, if you have evidence that some analyst's earnings forecasts have influence on a stock/index, your model would probably be more about the analyst than actual earnings.

Edit 1 (10/11/2011) ===================================================

Additional information on IBES earnings data:

http://www.olin.wustl.edu/docs/Faculty/Larocque%20paper.pdf

Analyst earnings expectations:

http://rady.ucsd.edu/faculty/directory/timmermann/docs/three_states_24May_2009_final.pdf

http://business.rice.edu/uploadedFiles/Faculty_and_Research/Academic_Areas/Accounting/papers/yeung_january_2011.pdf

http://www.stanford.edu/group/knowledgebase/cgi-bin/2011/08/15/when-they-are-wrong-analysts-may-dig-in-their-heels/

http://www.business.uconn.edu/Realestate/publications/pdf%20documents/407%20Do%20Investors%20See%20Through%20Mistakes%20in%20Reported%20Earnings.pdf