I am seeing an issue when callibrating an MP distribution. Assume a log return series for the SP500 with the following dimensions

dim(xts.sp500.ret.stocksonly)

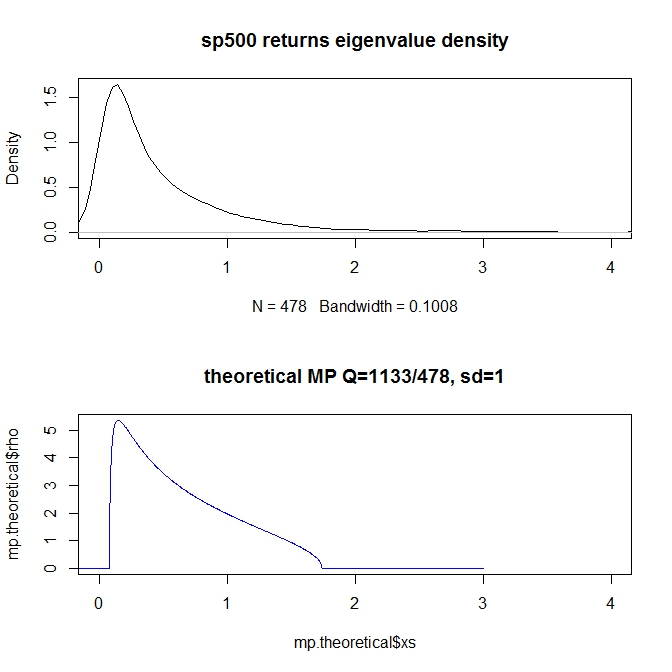

==> [1] 1133 478

sp500.cor <- cor.empirical(xts.sp500.ret.stocksonly)

sp500.eigens <- eigen(sp500.cor)$values

sp500.eigen.density <- density(sp500.eigens,n=5000)

plot(sp500.eigen.density,xlim=c(0,4),main="sp500 returns eigenvalue density")

I assume my 'Q' value is 1133/478 =

Problem: Even though the 'shape' and cutoffs seem OK -- the density value (y axis) seem vastly OFF. Peak of 1.5 for the real series - 5 or so for the theoretical, (note I am truncating the plot so the market eigenvalues are not shown, they are huge around 200).

Question: 1) Is this expected? 2) How does this affect callibration? Should I trust the results and simply look at the cutoffs? 3) Also when 'cleansing' the matrix I see most code (e.g. filter.RMT in tawny) simply replaces values below Lambda+ with the average, what about Lambda- though?

thanks much!