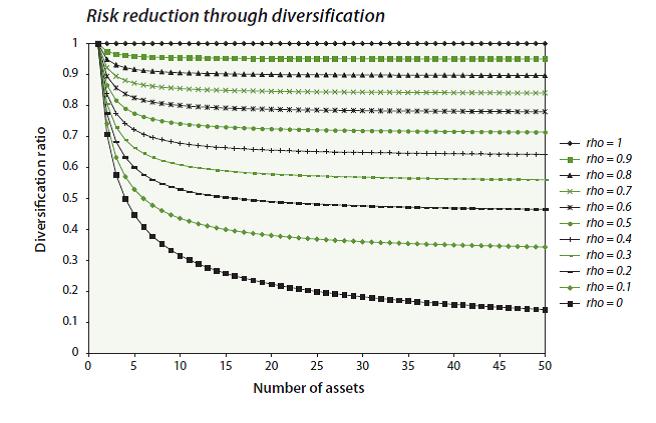

I have seen multiple instances where people try to explain the diversification effects of having assets with a certain level of correlation, especially in the "most diversified portfolio" literature. A nice example is in the NewEdge's "Superstars vs. Teamwork":

How can I simulate multiple random walk series that have a calibrated level of correlation to each other in order to demonstrate this? My thought is to have a random walk series $x$ and to add varied different levels of noise $n$.

$$r_i = \lambda x + (1 - \lambda) n_i$$

where $$0 \le \lambda \le 1$$

So less noise (large values of $\lambda$) will generate series with high correlation vs. more noise. But is there are more theoretical way to calibrate a certain level of correlation? I'm simulating this in R, so any R functions would be additionally helpful!