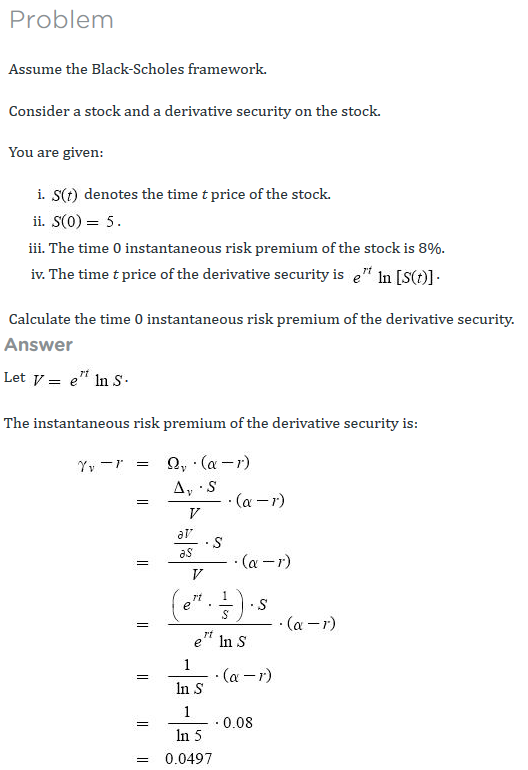

I understand the author's intended solution to the below problem, but I thought I would see if I could solve this using first principles and Ito's Lemma instead for practice.

Let $V(S(t), t) = e^{rt}\ln{[S(t)]}$. Then

\begin{align*}V_S &= \frac{e^{rt}}{S(t)},\\ V_{SS} &= \frac{-e^{rt}}{[S(t)]^2} \text{, and}\\ V_t &= re^{rt}\ln[S(t)].\end{align*}

Assuming the Black-Scholes framework, $dS(t) = (\alpha - \delta)S(t) dt + \sigma S(t) dZ(t)$. By Ito's Lemma,

\begin{align*}dV &= (\alpha - \delta)e^{rt} dt +e^{rt}\sigma dZ(t) - \frac{1}{2}e^{rt}\sigma^2 dt + re^{rt}\ln[S(t)]dt\\ &=[(\alpha - \delta)e^{rt} - 0.5e^{rt}\sigma^2 + re^{rt}\ln[S(t)]dt + e^{rt}\sigma dZ(t).\end{align*}

It would appear that without knowing anything about $\delta$ or $\sigma$, we have no where to go. So is there not a way to solve this problem from first principles without knowing that since the Sharpe ratios of the asset and the derivative are perfectly (positively) correlated, they are equal? I.e.,

$$\frac{\gamma_V - r}{\sigma_V} = \frac{\gamma - r}{\Omega_V\sigma} = \frac{\alpha - r}{\sigma},$$

where $\gamma_V$ is the continuously compounded return on the derivative and $\Omega_V$ is the elasticity of the derivative.