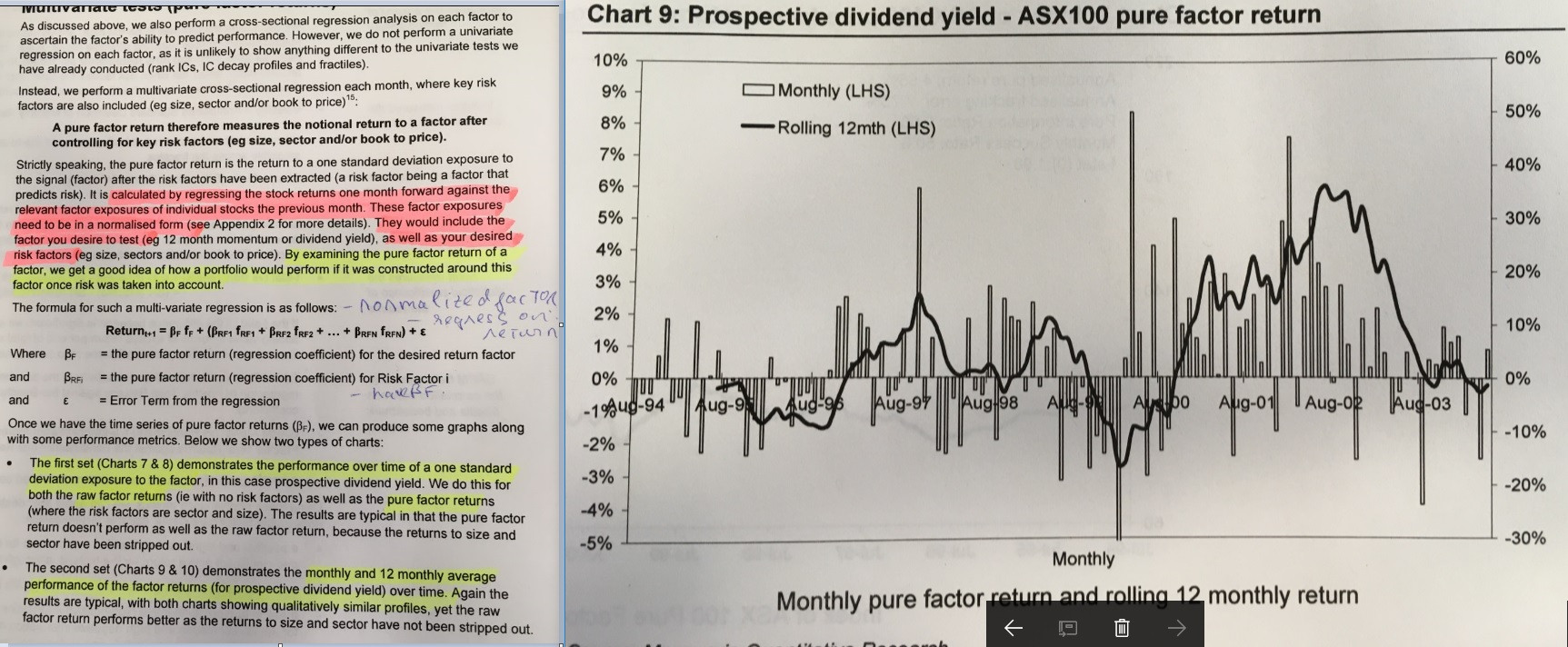

I am reading a paper. The authors use the multivariate regression to calculate the pure factor return $\beta_F$ using the following equation: $$Return_{t+1}=\beta_F f_F + \beta_{RF_1} f_{RF_1} +⋯+ \beta_{RF_N} f_{RF_N} +\epsilon$$

where

$\beta_F$ = pure factor return for the desired return factor,

$\beta_{RF_i}$ = pure factor return for Risk factor $i$,

$f_F$ = evaluated factors (ex: Dividend Yield)

$f_{RF_i}$ = risk factor (ex: size)

After that, they produce a monthly factor return as the graph here. I just wonder from the pure factor return for the desired return factor, how they can get the return over months like the graph?