You are right that there are limit and market orders and nothing else. But I'll clarify it. Market orders do not stay in the order book because they instantaneously matched against limit orders and generate trades. Limit orders depending on their limit price can also be instantly matched fully or partially. So, do you refer to aggressive orders in general (limit or market) or orders that are Market by type?

In any case, each exchange has its own way / data format to inform about it. Plus, data vendors (e.g. algoseek) may also post-process the data and convert it to another format. In this case it's necessary because algoseek needs to provide the data of the same symbols from different exchanges in a uniform format. As you can see below they don't do it very effectively, but it's up to them.

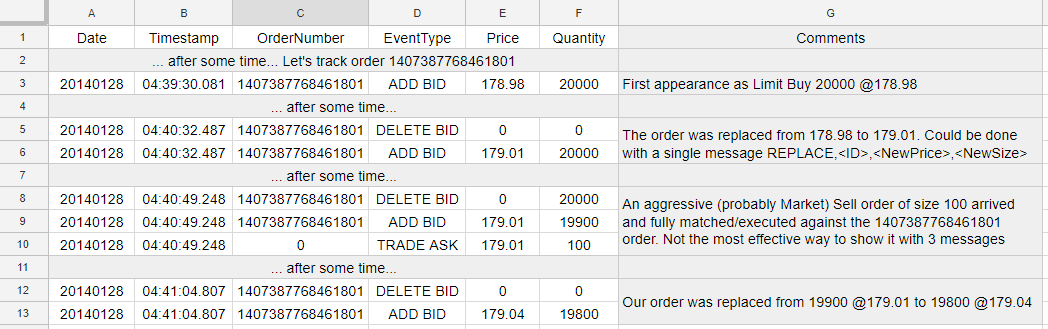

The documentation of the sample data seems to be outdated, but it's easy to guess the format from the content. So, in order to get Market orders or aggressive limit orders from the data or you need to analyse the trades. Here is an example. To make it more compact I removed the columns of Exchange, MMID, and Symbol.

If you wish to see actual Market orders in the data when they arrive, check GDAX data, see the description of the full channel in the API. Here is a short sample of the raw data. Each line starts with a timestamp (set by recording device).

Also, I highly recommend reading this crash course on Market Mechanics to clarify all the above and much more.

To summarize, any trade that you see in the market data is caused either by a Market order or by an aggressive (crossing the spread) Limit order. Basically, you can model a Market order as an aggressive Limit order with limit price deep in the opposite side.

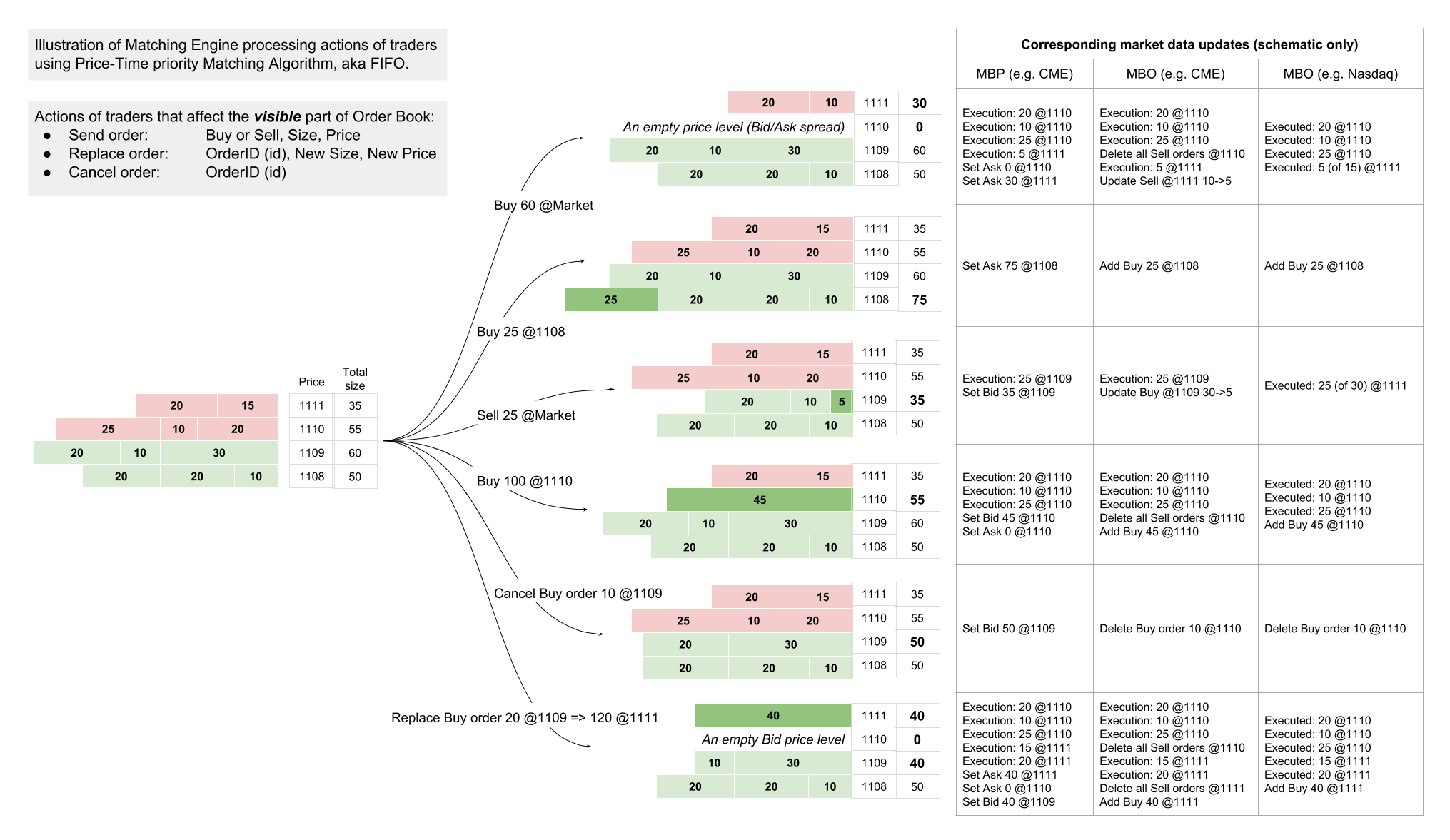

In some cases like with GDAX data you can see explicitly the type of the order that caused a trade, in some cases you can't see it. And in some cases you can back-engineer they type of the order based on the sequence of data updates. It allows to distinguish partially executed limit orders from market orders and fully executed limit orders. See case #4 from top on this diagram from the Market Mechanics article: