Yes, two different set of returns can lead to the same weights (so you won't be able to prove the opposite). Also, the term "unique solution" means something different than how you used it.

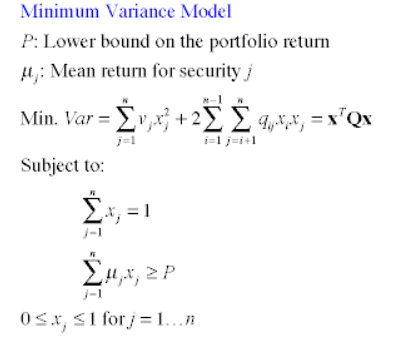

Taking $p$ and $Q$ as given, the mapping from $\boldsymbol{\mu}$ to solutions $\mathbf{x}^*$ is not injective

I'll give a simple counterexample that shows the mapping isn't injective. Let's assume $p=2$. $Q$ can be anything. Now consider two scenarios:

- Scenario 1: $\boldsymbol{\mu} = \begin{bmatrix} 1 \\ 3 \end{bmatrix}$

- Scenario 2: $\boldsymbol{\mu} = \begin{bmatrix} 0 \\ 4 \end{bmatrix}$.

The solution to your above optimization problem in both cases is $ x= \begin{bmatrix}.5 \\ .5 \end{bmatrix}$. Two different inputs map to the same output, hence the mapping isn't injective.

What's going on?

If you have $k$ assets, vector $\boldsymbol{\mu}$ lives in a $k$ dimensional space. On the other hand, the constraints on $\mathbf{x}$ imply that solution $\mathbf{x}^*$ can only take values in a $k-2$ dimensional space. You're not going to have a one to one correspondance between spaces of different dimension.

What people mean by unique solution

When people say an optimization problem has a unique solution, they mean it has a solution and the solution is unique.

They do not mean that the mapping from optimization problem inputs to optimal choice variables is an injective function.