First and foremost, I'm trying to understand why you would construct a portfolio made up of long calls, long puts and short calls. I find this really abstract and confusing. I've tried drawing the pay-off diagram but I can't wrap my head around it. Does anyone have an intuitive explanation as to when this might be useful and under what market conditions?

I've been asked to calculate the Delta, Gamma and Delta-Gamma approximation for the PL in terms of the underlying return $R$. As usual, $S$ is the underlying asset price, $K$ is the strike price, $r$ is the risk-free rate, $\sigma$ is the volatility, $T$ is maturity and $\Phi$ is the standard normal distribution function.

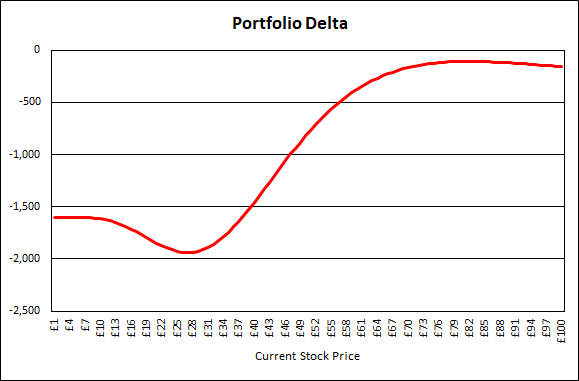

Let's say the portfolio is made up of the following:

- Long $3,000$ call options with strike $K=52$ and expiry $T=6m$ ($\Delta_1$)

- Long $1,600$ put options with strike $K=48$ and expiry $T=3m$ ($\Delta_2$)

- Short $4,000$ call options with strike $K=56$ and expiry $T=1y$ ($\Delta_3$)

All options have the same underlying $S$. The current asset price is $S_0=50$, $\sigma=25\%$ and $r=5\%$.

The Delta is a pretty straight-forward plug in of the numbers into:

$\Delta_{call} = \Phi(d_1)$, where $d_1=\frac{\ln\left(\frac{S}{K}\right)+(r+\sigma^2/2)T}{\sigma \sqrt{T}}$

However, this is where I get confused. The Delta of the long calls ($\Delta_1$) is just a straight-forward plug-in of the numbers. The Delta of the long puts ($\Delta_2$) is equal to $\Delta_{call}-1$ through put-call parity. What I get confused about is the $\delta$ for the short calls. In this instance, $d_1$ is negative, however, $\Phi(d_1)$ is the cdf for the standard normal so is always between $0$ and $1$, meaning the Delta is positive, and as we are short, the Delta term is negative.

In my head this is: $\Delta_{portfolio} = +\Delta_1 +\Delta_2 - \Delta_3$ (long, long, short), which leads to a negative delta for the portfolio as $\Delta_1$ is positive, $\Delta_2$ is negative and $\Delta_3$ is positive.

I get that a negative Delta is advantageous in a bearish market when the underlying is expected to go down but this particular portfolio structure has my head spinning. Once I have my head around the Delta I'm sure I can do the rest but I'm struggling to understand this even on a basic level. The different time horizons add to the confusion so any intuitive explanation around that would also be welcome.