This is what I've got, but I'm getting weird results. Can you spot an error?:

zciisData = [(ql.Date(18,4,2020), 1.9948999881744385),

(ql.Date(18,4,2021), 1.9567999839782715),

(ql.Date(18,4,2022), 1.9566999673843384),

(ql.Date(18,4,2023), 1.9639999866485596),

(ql.Date(18,4,2024), 2.017400026321411),

(ql.Date(18,4,2025), 2.0074000358581543),

(ql.Date(18,4,2026), 2.0297999382019043),

(ql.Date(18,4,2027), 2.05430006980896),

(ql.Date(18,4,2028), 2.0873000621795654),

(ql.Date(18,4,2029), 2.1166999340057373),

(ql.Date(18,4,2031), 2.152100086212158),

(ql.Date(18,4,2034), 2.18179988861084),

(ql.Date(18,4,2039), 2.190999984741211),

(ql.Date(18,4,2044), 2.2016000747680664),

(ql.Date(18,4,2049), 2.193000078201294)]

def build_inflation_term_structure(calendar, evaluationDate):

dayCounter = ql.ActualActual()

yTS = build_yield_curve()

lag = 3

fixing_date = calendar.advance(evaluationDate,-lag, ql.Months)

convention = ql.ModifiedFollowing

cpiTS = ql.RelinkableZeroInflationTermStructureHandle()

inflationIndex = ql.USCPI(False, cpiTS)

#last observed CPI level

fixing_rate = 252.0

baseZeroRate = 1.8

inflationIndex.addFixing(fixing_date, fixing_rate)

observationLag = ql.Period(lag, ql.Months)

zeroSwapHelpers = []

for date,rate in zciisData:

nextZeroSwapHelper = ql.ZeroCouponInflationSwapHelper(rate/100,observationLag,date,calendar,

convention,dayCounter,inflationIndex)

zeroSwapHelpers = zeroSwapHelpers + [nextZeroSwapHelper]

# the derived inflation curve

derived_inflation_curve = ql.PiecewiseZeroInflation(evaluationDate, calendar, dayCounter, observationLag,

inflationIndex.frequency(), inflationIndex.interpolated(),

baseZeroRate, yTS, zeroSwapHelpers,

1.0e-12, ql.Linear())

cpiTS.linkTo(derived_inflation_curve)

return inflationIndex, derived_inflation_curve, cpiTS, yTS

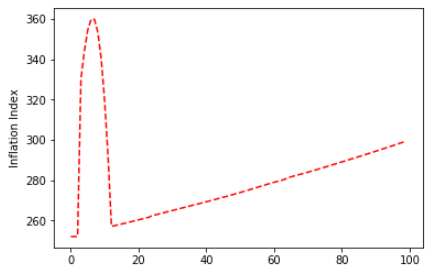

If I plot the inflationIndex zero rates, I get this: