I read that recently, due to the covid-19, the pressure on the dollar market has risen significantly on the demand side. That is why the dollar basis became largly negativ.

https://www.bloomberg.com/news/articles/2020-03-17/how-cross-currency-basis-swaps-show-funding-stress-quicktake https://www.bis.org/publ/bisbull01.pdf

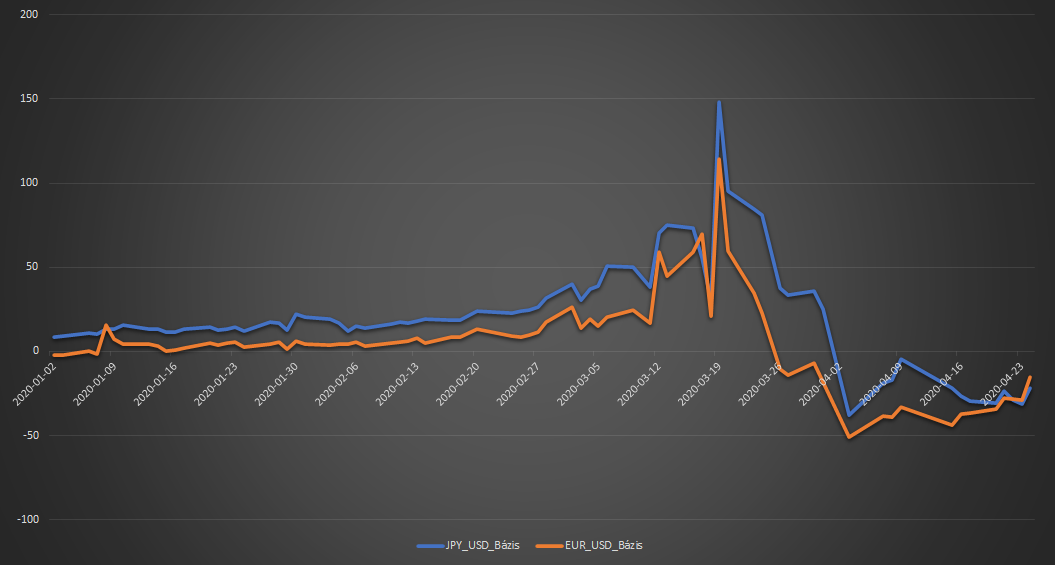

I tried to replicate this calculation for a university Essay. From the spot and 3M fwd rate I calculated the implied dollar interest rate. Then for the basis from this I extracted the 3M USD LIBOR.

However my graph is looking like this: It seems to me pretty the same, but on the positive side. Do I misinterpret it, if I say, it shows the premium which I have to pay, due I don't have access to direct us market, so I finance through the off-shore dollar market?

Could someone explain me, whether I misunderstood something or am I using the wrong dataset.

Thank you!

It seems to me pretty the same, but on the positive side. Do I misinterpret it, if I say, it shows the premium which I have to pay, due I don't have access to direct us market, so I finance through the off-shore dollar market?

Could someone explain me, whether I misunderstood something or am I using the wrong dataset.

Thank you!