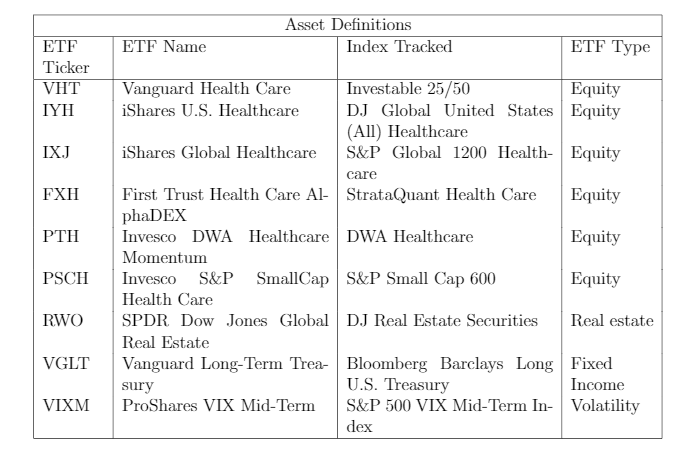

I have the following portfolio of all ETFs:

I am attempting to apply Black Litterman and on the step of calculating market weights. I have the following questions:

How can I define what index to use as a benchmark? ( Is it the average of all index tracked? and then use that as my market universe)

How can I define what to use as the market weights for this to find the Implied equilibrium returns? (is it just mcap etf/total mcap of all ETF's)

Any formulas for the above questions would be great. Thanks in Advance