I've been trying to calibrate Hull-white one factor model with swaption but I have a trouble making closed form solution of swaption

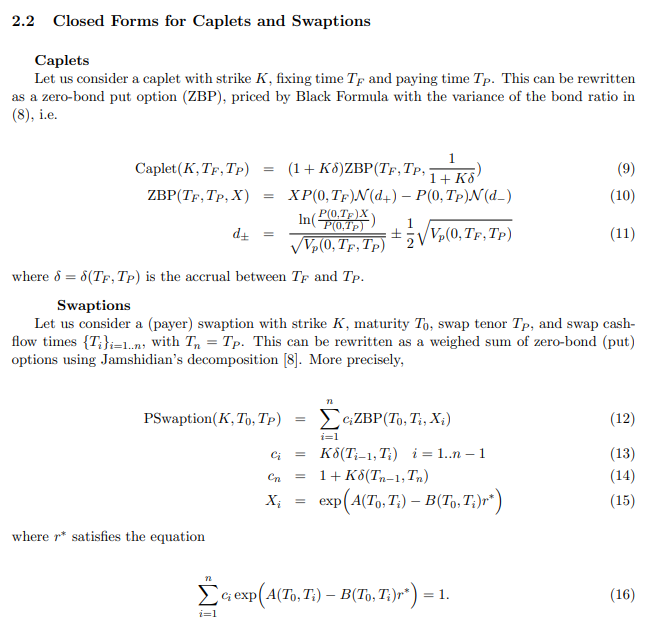

Below is the part of paper I've been referencing to

https://people.kth.se/~aaurell/Teaching/SF2975_HT17/calibration-hull-white.pdf

The problem is r* part.

In order to calculate the price of swaption following the instruction of the paper, I need to solve the equation (16) to come up with r*.

But it seems that there is no closed-form solution to this equation finding r*.

However, if no closed-form solution exists for pricing swaption, the whole calibration process takes too long. I think it is not what the author intended.

Is there any closed-form solution for finding r* in this equation?

Many thanks in advance for helping me.