It's a good question, if only because it's about a bad assertion that conflates related concepts!

The easiest answer to your question is the argument that "if the market isn't tangency, then everyone would do tangency, pushing the market to tangency". Which is just a basic re-hashing of all the standard arguments about market efficiency.

One obvious pushback (to which, I think, you allude) is that this does not follow; but in the absence of reliable evidence of mispricing, I have no better prior for any stock's valuation than its market valuation. Semi-strong efficiency 101, in the jargon. I believe therefore that market equals or approximates tangency, because I have no superior prior.

But this argument cannot neatly reconciled with "supply and demand" ;-) Because supply and demand are both conditioned by price. What is the supply at price X; what is the demand at the same price X. It follows there will be a difference at price equals not-X. X being a function of expected return, for simplicity's sake.

Then ask yourself whether X has to be the same for every stock in the market. This is not true; and it's even axiomatic to standard market theory. This says that if we floated "Ladca & DEM's Speculative Punts in New Crypto Inc" on the NASDAQ tomorrow, our little levered venture would probably have a higher cost of capital than the Dow Jones. You could rationalise this fact, either through a higher WACC fundamental argument or though a technical CAPM higher vol equals higher beta one. In any language, two people who have never met punting i-coins by flipping coins is not like Amazon, Proctor & Gamble, or Bank of America.

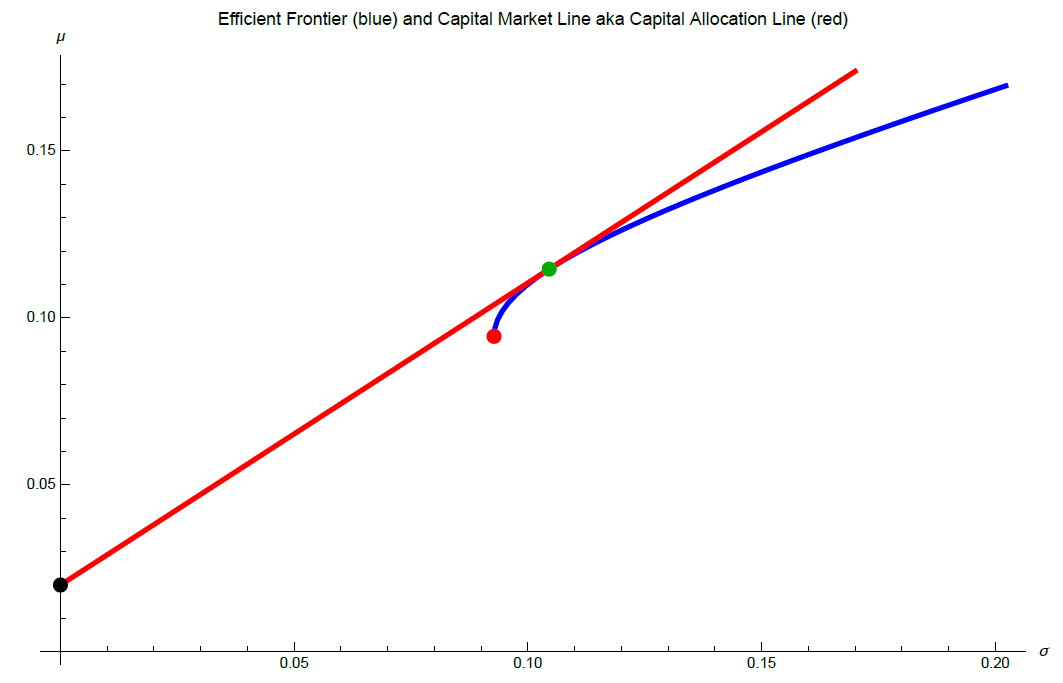

Our stock would thus require a higher return to attract demand; and create higher supply at a lower rate of return. Irrespective of our correlation to AMZN, PG, and/or BAC, this at a stroke invalidates the tangency=market argument. Because the tangency portfolio could choose to run a small-cap bias that generates a higher return than an index with concentrated exposure to mega-caps, without this necessarily creating an equal-and-opposite volatility.

It might be higher "risk"; but the "risk" there is not an optimised return slope to vol. The argument you're asking about is, in my opinion, intellectually lazy BS. I wouldn't lose sleep over it.

best,

DEM

[ps if you don't believe this, ask yourself how the bond market (as big as the equity market, larger if you include credit) can function with yield curves where volatility is an almost linear function of duration, but the compensation for this risk is linear maybe 1% of the time. Different kinds of volatility can be differently priced; just as different kinds of profitability can be. Drawing straight lines through "return" and "vol" is thus wrong to begin with]