I think it's best to start with explaining what the VIX actually is, because I think afterwards it will be clear(er) why indices like that don't exist for everything you ask for (or are not usually used).

The VIX index is theoretically the square root of the variance swap strike and computed via SPX options that are listed for trading on the Cboe. Once you understand that VIX is akin to Variance swaps, you will probably realise it makes little sense to talk about a VIX for real estate or cash.

For credit, interest rates and commodities, it helps to look at how the fair value of a variance swaps is computed as the integral of weighted prices of out-of-the-money options over all strikes. One obvious problem here is that options markets are composed of a discrete set of option prices for a given maturity. Due to these practical difficulties in replicating the actual log payout across strikes, the market for equity index varswaps usually trades at a basis to the replicating portfolio. SPX however is very liquid and has a huge range of strikes.

Credit, and interest rates are a completely different beast. This article by ANTONIO MELE AND YOSHIKI OBAYASHI offers a concise explanation why variance swaps are more complex in the FI world. For example, you can have yield vol, as well as price vol. The MOVE index measure yield vol computed computed with the following weights: 20% 2-Yr, 20% 5-Yr, 40% 10-Yr and 20% 30-Yr. Supposedly 10-Yr is overweight as it is the benchmark maturity for OTC options (based on volume estimates at the time of creation). TYVIX measured price vol (which is a lot less common).

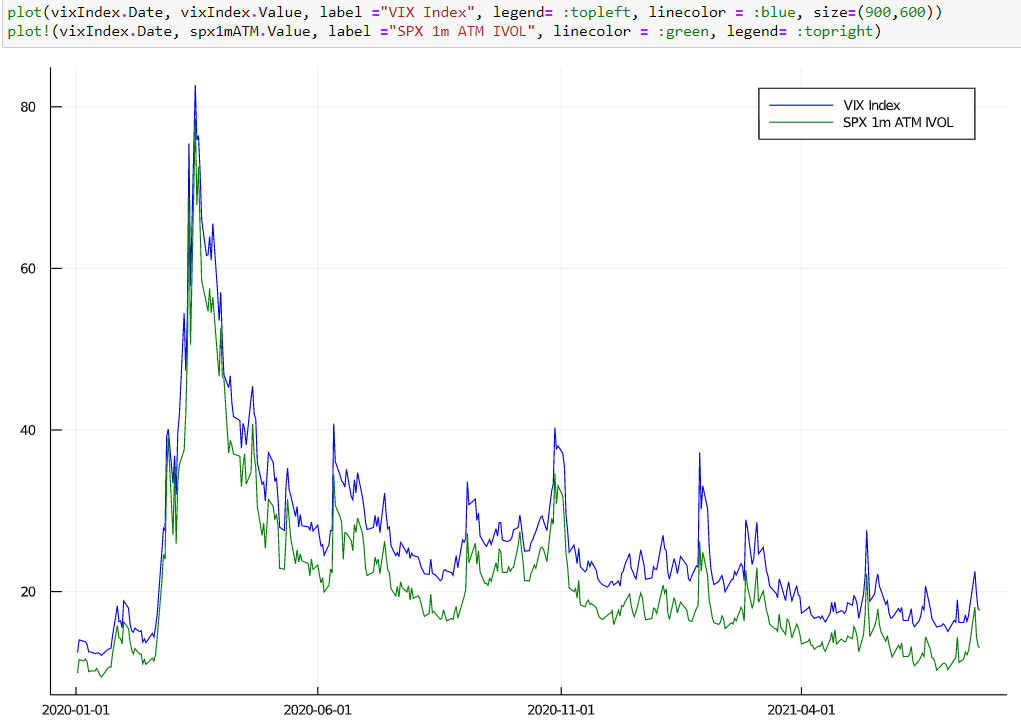

FX, for example, is generally quoted in IVOL. So in FX, with a well defined vol surface there is usually little need for VIX type computations. You can look at this answer to see that VIX is not very different from a "simple" 1m ATM vol (in value, not in how it is computed). Below is a comparison, where the 1m ATM vol comes from a vol surface.

In my opinion, before you try to simply find stuff that is "similar" to VIX, I think it may be best to ask yourself first why you would want that? VIX is marketed by the CBOE as the market’s expectation of future volatility. However, neither IVOL, nor the (square root of the) fair strike of a variance swap are truly expectations of realized volatility. Wikipedia's VIX page shows that the VIX has virtually the same predictive power as past volatility alone.

If you simply want to measure "uncertainty", it is completely sufficient to look at ATM IVOL (as shown in the chart above).

That said, the CME is building CVOL (Scroll down to see a short video). This indices exist for all sorts of asset classes (also in the link).