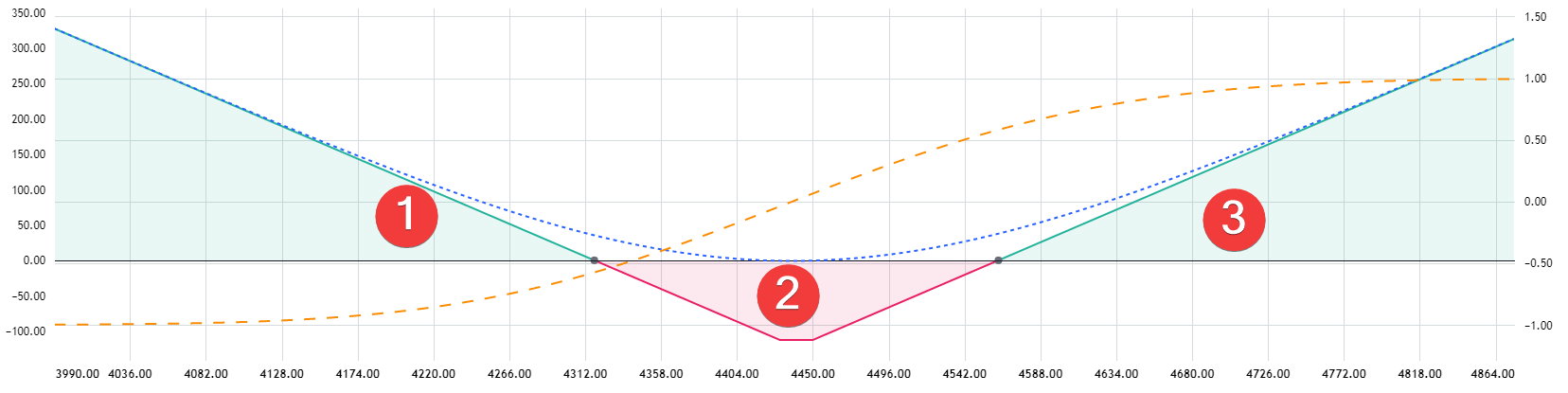

Big picture

For any options strategy, for any segment between zero profit (breakeven) points, I want to calculate probabilities of the underlying instrument price will be within a segment at expiration. On the illustration, I want to know probabilities for segments 1,2 and 3.

My environment

- No time series of the underlying instrument price available. So I don't consider approaches where I have to fit real distribution with something like Student.

- Analitical form of a volatility curve is available.

The approach that is on my mind

- For each breakeven point calculate a delta of a virtual option with a strike at this point. Can do this since I have analitycal IV curve.

- Each of these deltas can be interpreted as a probability of underlying price is higher then corresponding breakeven point at expiration

- Having array of these probabilities, I can calculate probabilities for segments.

My questions

- Is my approach generaly acceptable?

- What are another approaches you might advise?