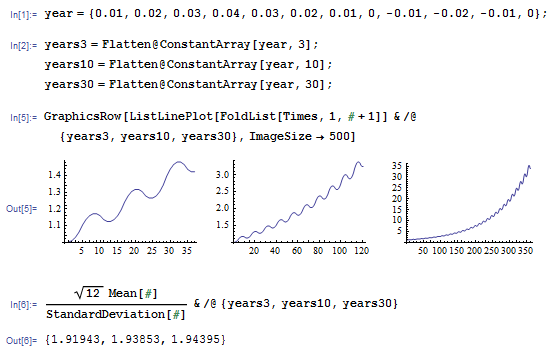

I try to understand why a $\sqrt{252}$ normalization factor is useful for Sharpe Ratio:

Let's compute the Sharpe Ratio for this imaginary portfolio, for various sampling periods:

import numpy as np

import matplotlib.pyplot as plt

T = 252 # 252 days ~ 52 weeks of 5 days ~ 12 months of 21 days

for period in [1, 5, 21]: # sample every 1 day, 1 week, or 1 month

x = np.arange(0, T, period)

y = 100 + x + 3 * np.sin(x)

returns = (y[1:] / y[:-1] - 1) # will be daily, weekly, monthly returns

plt.plot(x, y)

plt.show()

plt.plot(returns)

plt.show()

print 'Sharpe Ratio: %.5f' % (np.sqrt(T/period) * returns.mean() / returns.std())

# sqrt(T/period) is sqrt(252), ~ sqrt(52), sqrt(12)

Results

I get something nearly constant :

Sharpe Ratio: 7.24790

Sharpe Ratio: 10.49590

Sharpe Ratio: 7.84525I find this really coherent and good because for these 3 sampling rates, the ratio is similar: it doesn't depend on the sampling rate** but is intrinsic to the portfolio itself.

Question :

I see this is coherent. But why this normalization factor in Sharpe Ratio?