Here's an interesting trading puzzle that I would love to get the community's input on.

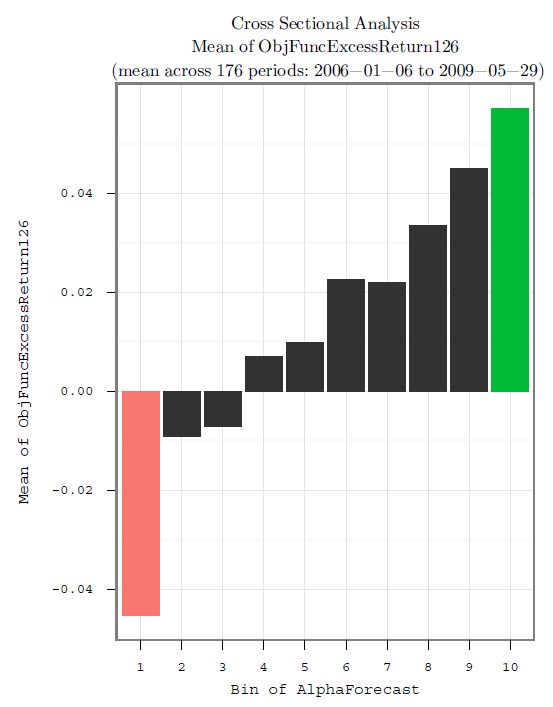

Let's say there exists an alpha signal that does a good job of sorting equities expected excess returns over some number of weeks. If we bin the alpha forecast into 10 equally sized frequency bins, we find that bin 1 has the lowest (and negative) mean realized excess return and bin 10 has the highest (and positive) mean realized excess return. The middle bins have middling risk-adjusted returns and there is nice monotonic pattern on average over non-overlapping periods as in the chart below:

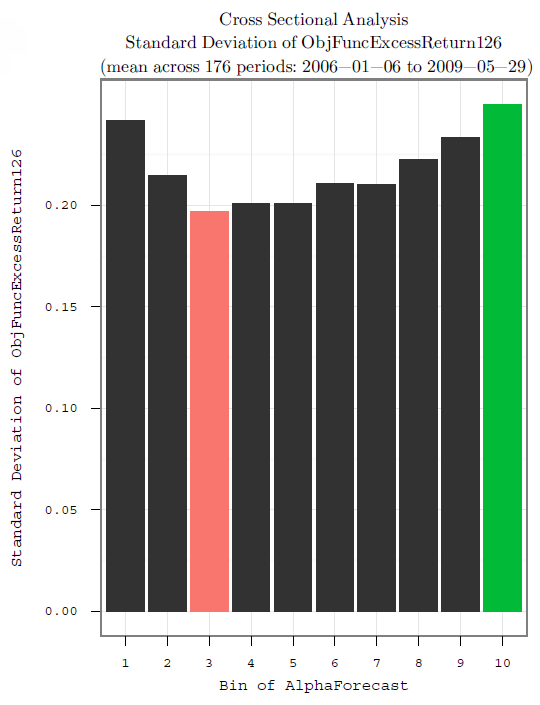

It also turns out that empirically the bins with smaller expected alpha also have lower realized volatility as depicted in this chart:

As you can see there is considerable variance of returns in any given bin that the mean summary metric obscures.

A typical market-neutral approach is to go long bin 10 and short bin 1, or simply drop all the forecasts into an optimizer since you have a nice monotonic pattern. That's all well and good but it leaves signal on the table. The weights produced via a typical approach will understandably not take significant large long/short positions in the middling bins despite the fact that there is considerable information in knowing that these securities have lower volatility and middling returns.

My question is how to best exploit the signal in the middling bins? How to best exploit the ability to separate securities by their expected realized volatility? For example, maybe one strategy is to generate premium income by writing straddles on the middle bins or somehow trade the volatility of one bin against another? It seems that the volatility on the tail bins are under priced, and the vol on the middle bins may be overpriced. Unfortunately, I do not have a similar chart showing the implied volatility for the various bins but they are all components of the S&P 500 so strategies relative to the Vix might be suitable.

Note, these are mean risk-adjusted excess returns (with respect to the S&P 500 benchmark) so total returns may be all positive or all negative during turbulent periods. Ideally, I'd like to avoid introducing market exposure, net market vol exposure, or other unhedged risks except for exposure to the alpha signals or realized volatility estimates themselves.

Thoughts?