I got the following interview question and corresponding solution, but I have a different understand that might be wrong, so I really appreciate your advice on it:

A European put option on a non-dividend paying stock with strike price 80 dollars is currently priced at 8 dollars and a put option on the same stock with strike price 90 dollars is priced at 9 dollars. Is there an arbitrage opportunity existing in these two options?

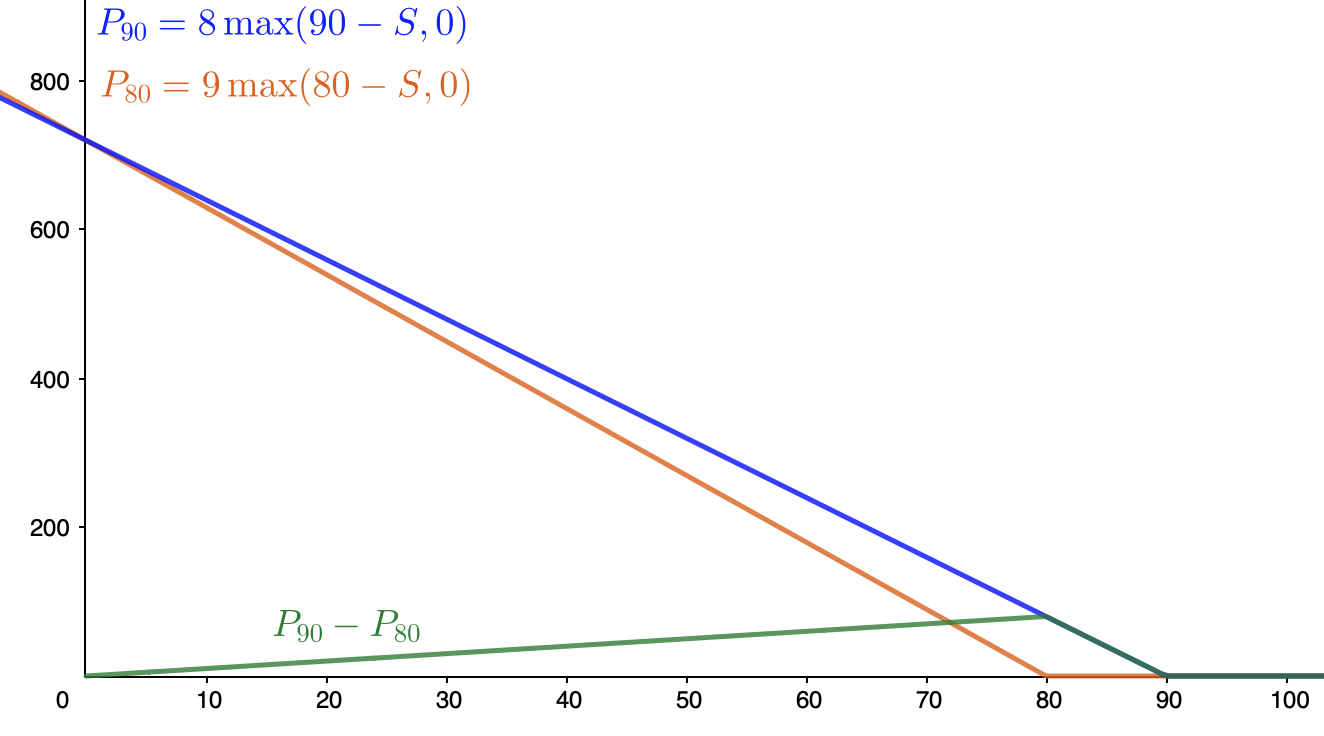

Solution: since the price of a put option as a function of the strike price is a convex function, and since a put option with strike 0 is worthless, we always have $P(0)+aP(K) = aP(K)>P(aK)$. So we have: $(8/9)*P(90) = (8/9)*9 = 8>P(80)$ Since the put option with strike price 80 dollars is currently priced at 8, it is overpriced and we should short it. The overall arbitrage portfolio is to short 9 units of put with $K=80$ and long 8 units of put with $K=90$. At time 0, the initial cash flow is zero. At maturity date, we have three possible scenarios:

$S_T>=90$,payoff=0 (no put is exercised)

$90>S_T>=80$, payoff = $8*(90-S_T)>0$ (puts with K=90 are exercised)

$S_T<80$, payoff = $8*(90-S_T)-9*(80-S_T)>0$ (all puts are exercised)

The final payoff $>=0$ with positive probability. So it is clearly an arbitrage opportunity.

But can I understand the question as follows?

I think the put option with strike 80 is underpriced (instead of overpriced), why? because: by using $aP(K)>P(aK)$ mentioned above, we have:$(9/8)*p(80)>=p[(9/8)*80]=p(90)=8$ So we have $P(80)>=8$, so it is under priced. I'm wondering if I'm wrong?