The problem I am looking at concerns the treatment of almost identical assets in portfolio construction.

Let us assume that we have two assets, both with a standard deviation $\sigma=0.2$ and a correlation matrix $$ C = \begin{pmatrix} 1 & 0.98 \\ 0.98 & 1 \end{pmatrix}. $$ One asset has a return of $\mu=0.101$ and the other has a return of $\mu=0.1$.

An argument usually employed in justifying portfolio construction models is that as the two assets are almost identical, the allocation outcome does not matter and for example putting the full (or a large) allocation into the asset with the slightly higher return is perfectly reasonable.

However, setting aside any additional costs that might arrive from investing in two assets instead of one, in terms of guarding against estimation and model error it might be preferable to invest half the total allocation into each asset.

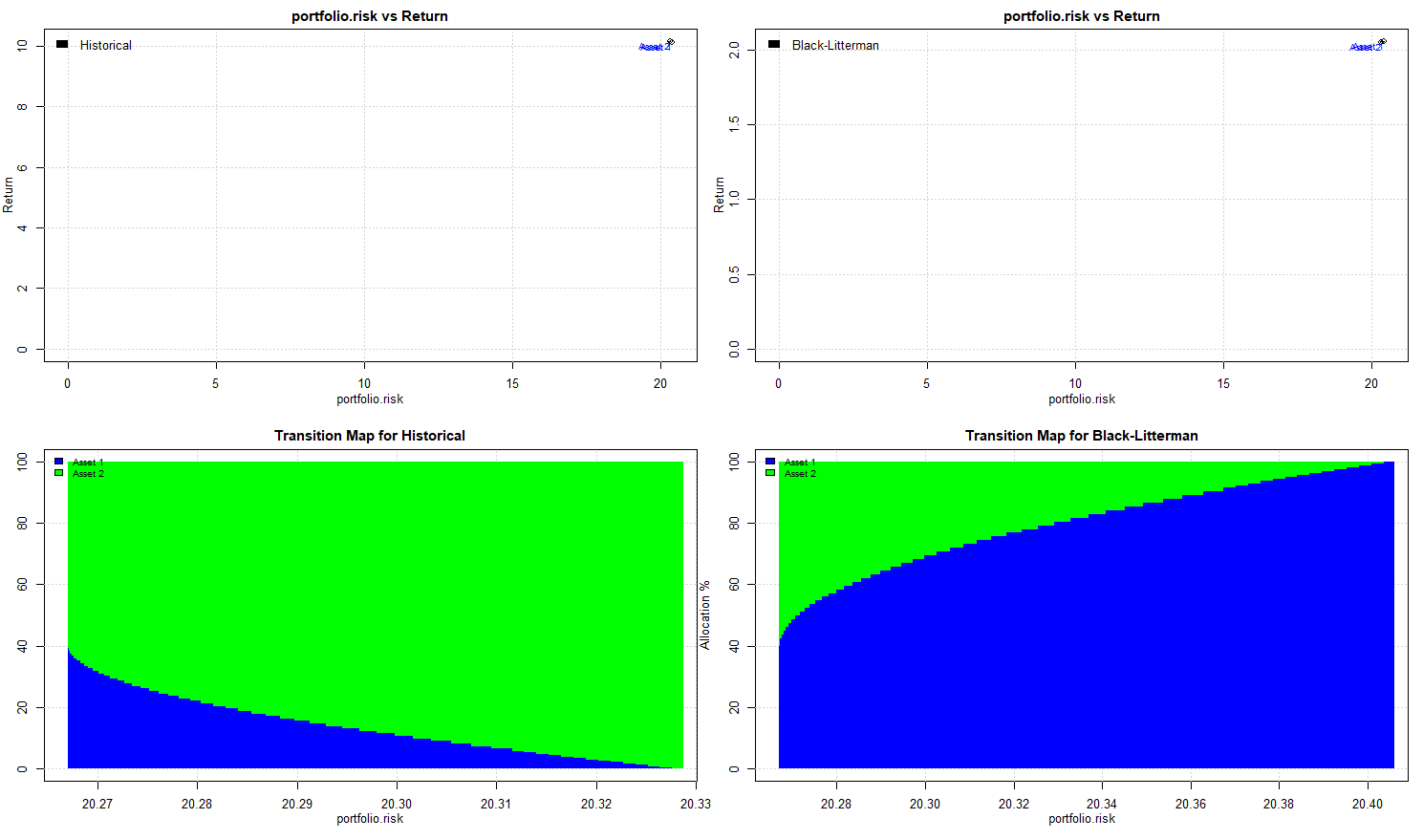

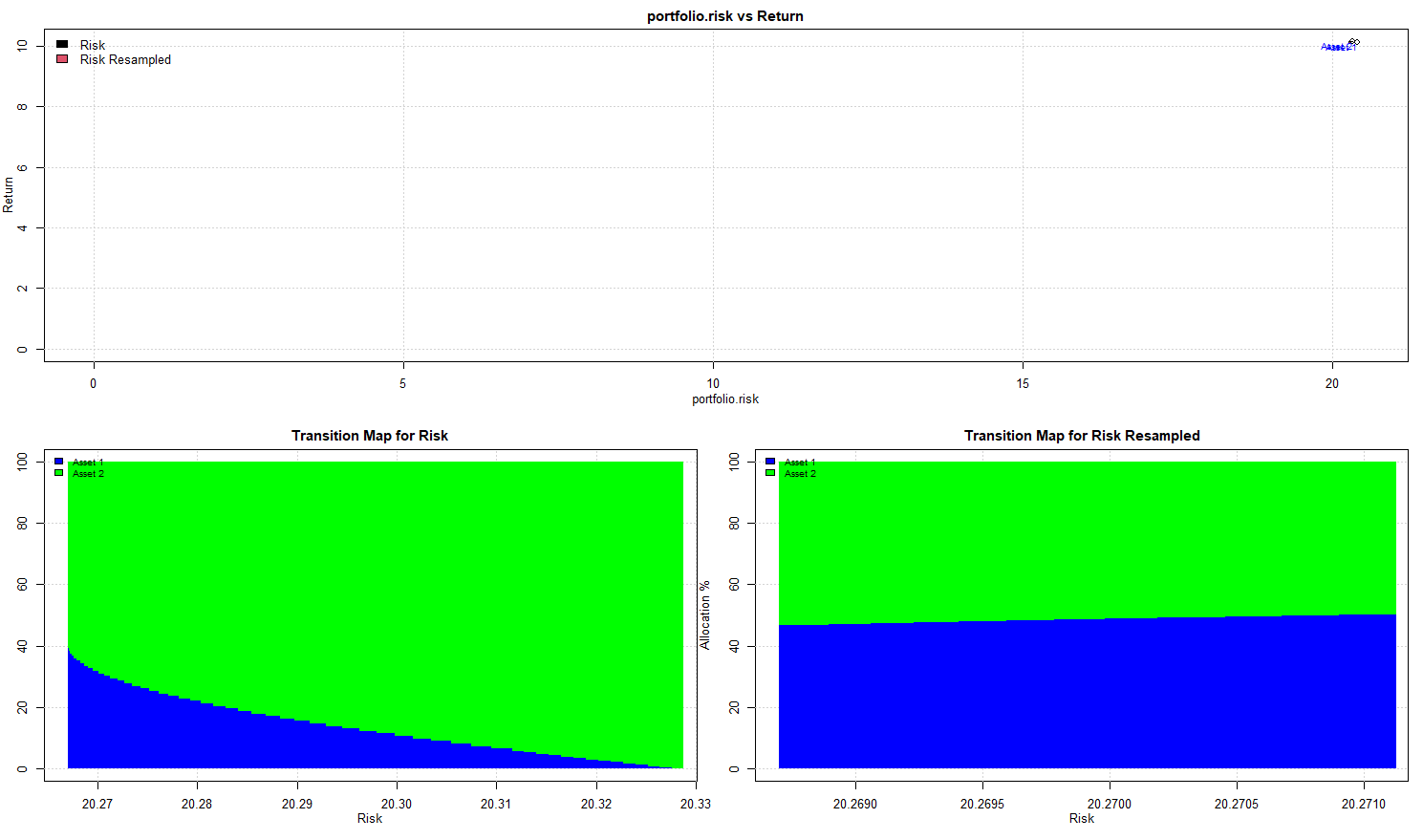

For the example above, I am showing below the results for Black-Litterman 1, 2 and the Resampled Efficient Frontier by Michaud 3, with the Mean-Variance solution as a reference (labelled historical) on the left-hand for both charts.

Black-Litterman

For the prior I have used the Equal-Risk-Contribution portfolio, which I understand is a deviation from the conventionally used market-equilibrium portfolio. The ERC weights are naturally 50%-50% for the assets. However, as Black-Litterman shrinks to the returns implied by ERC and not to the weights, the outcome is not a 50%-50% split at each level of risk.

Resampled Efficient Frontier

Due to the nature of the sampling, the resampled efficient frontier will produce weights that will always split approximately 50%-50%. However, unfortunately the REF has some other undesirable side-effects 6, among them increasing the weight of high-volatility assets when using a long-only constraint and reducing to the Mean-Variance solution when allowing shorting.

My question is: Is there a way to arrive at the behavior of the Resampled Efficient Frontier in the special case of two almost identical assets with either Black-Litterman or some other portfolio construction methodology? Is there a fundamental point that I am overlooking in this?

1 The Intuition Behind Black-Litterman Model Portfolios

2 A Step-By-Step Guide to the Black-Litterman Model Incorporating User-specified Confidence Levels

3 Estimation Error and Portfolio Optimization: A Resampling Solution

6 Resampled Efficiency and Portfolio Choice